|

|

Item No: GB.1 |

Ordinary Meeting of Council

TO BE HELD ON Tuesday, 26 February 2013 AT 7.00pm

Level 3 Council Chambers

Agenda

** ** ** ** ** **

NOTE: For Full Details, See Council’s Website –

www.kmc.nsw.gov.au under the link to business papers

DECLARATIONS OF INTEREST

Confirmation of Reports to be Considered in Closed Meeting

Address the Council

NOTE: Persons who address the Council should be aware that their address will be tape recorded.

Documents Circulated to Councillors

CONFIRMATION OF MINUTEs

Minutes of Ordinary Meeting of Council 9

File: S02131

Meeting held 5 February 2013

Minutes numbered 01 to 19

minutes from the Mayor

MM.1 2013 Australia Day Honours and Citizen of the Year Awards 54

File: S07765/4

I am pleased to inform you that 10 Ku-ring-gai citizens, through their outstanding achievements and services to the community, have been awarded 2013 Australia Day Honours.

We are very proud to have these dedicated and talented Australians as members of the Ku-ring-gai community.

I would like to read to you the names of these special Ku-ring-gai citizens and, on behalf Council, congratulate them on their excellent contributions to Australian society.

Philip BELL OAM of Wahroonga, for service to education, and to the community

Eftihia BLAND OAM of Turramurra, for service to the community through charitable organisations

Brian BOETTCHER AM of Wahroonga, for significant service to psychiatry as a clinician and educator

Stuart BOLAND AM of Killara, for significant service to medicine through leadership roles in professional organisations, and as a surgeon and educator

Brian BOYLE PSM (post-nominal) of West Pymble, for outstanding public service to Australian astronomy and for leadership of the Australian team bidding to host the international Square Kilometre Array facility

Ewen CROUCH AM of Roseville, for significant service to the law as a contributor to legal professional organisations, and to the community through executive roles with Mission Australia

Robert GEYER PSM (post-nominal) of EAST LINDFIELD, for outstanding public service to the development of the Chemical Analysis Branch, TestSafe Australia

Ronald HEINRICH AM of St Ives, for significant service to the law, and to the legal profession

Patrick MACMILLAN OAM of Wahroonga, for service to the community through Alzheimer’s Australia New South Wales

Pasquale PEDULLA OAM of Gordon, for service to the community through multicultural and aged care organisations.

I also congratulate Ku-ring-gai’s Citizen of the Year winners for 2013:

Citizen of the Year - Rohit Ralli

Young Citizen of the Year - Emma Gavaghan

Outstanding Service to the Community - Ian Eastman

Ku-ring-gai Environmental Award (individual) - Marjorie and Rolf Beck

Ku-ring-gai Environmental

Award (group) - The Australian Plant Society -

North

Shore Group

Ku-ring-gai Heritage Award - Kathie Rieth

On behalf of Council, I congratulate all these award winners on their outstanding achievements.

Ku-ring-gai should be proud that it has so many citizens being recognised at the highest levels for their selfless dedication, commitment and contribution to local, national and international communities.

Petitions

GENERAL BUSINESS

i. The Mayor to invite Councillors to nominate any item(s) on the Agenda that they wish to have a site inspection.

ii. The Mayor to invite Councillors to nominate any item(s) on the Agenda that they wish to adopt in accordance with the officer’s recommendation allowing for minor changes without debate.

GB.1 Model Code of Conduct 56

File: S06339

To adopt the new model Code of Conduct.

Recommendation:

That the latest version of the model Code of Conduct be adopted.

GB.2 Code of Meeting Practice 84

File: S02211

To consider a revised draft Code of Meeting Practice.

Recommendation:

That the revised Code of Meeting Practice be endorsed for placing on public exhibition in accordance with s.361 of the Local Government Act 1993.

GB.3 Privacy Management Plan 209

File: S05981

To adopt a revised Privacy Management Plan.

Recommendation:

That the revised Privacy Management Plan be adopted.

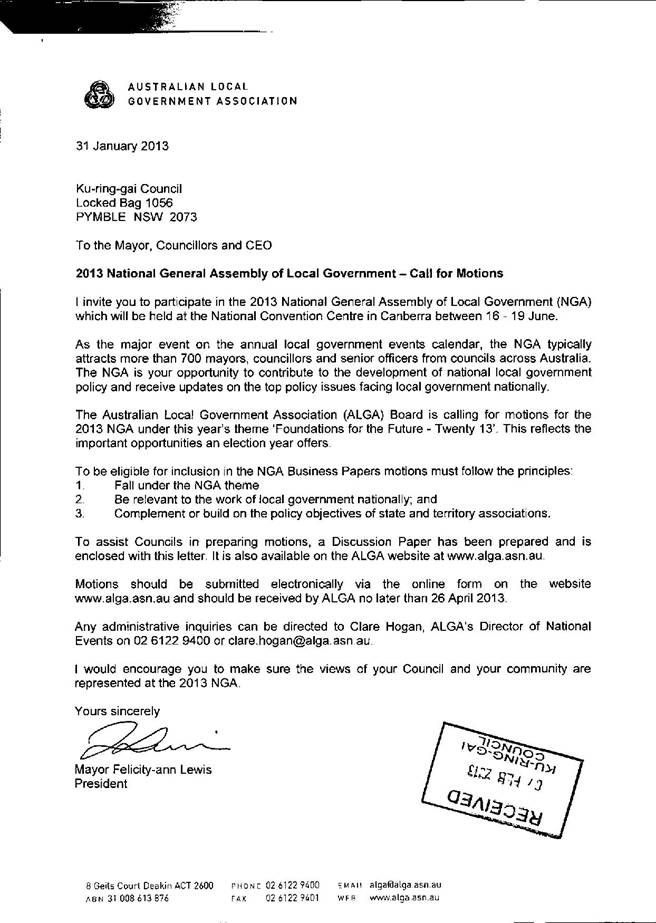

GB.4 2013 National General Assembly of Local Government - Call for Motions 281

File: S03788

To consider an invitation from the Australian Local Government Association (ALGA) to submit motions to the 2013 National General Assembly of Local Government.

Recommendation:

That Councillors consider whether they propose to submit any motions to the Conference and supply those to the General Manager by Friday, 22 March 2013 who will provide a further report to Council prior to the deadline.

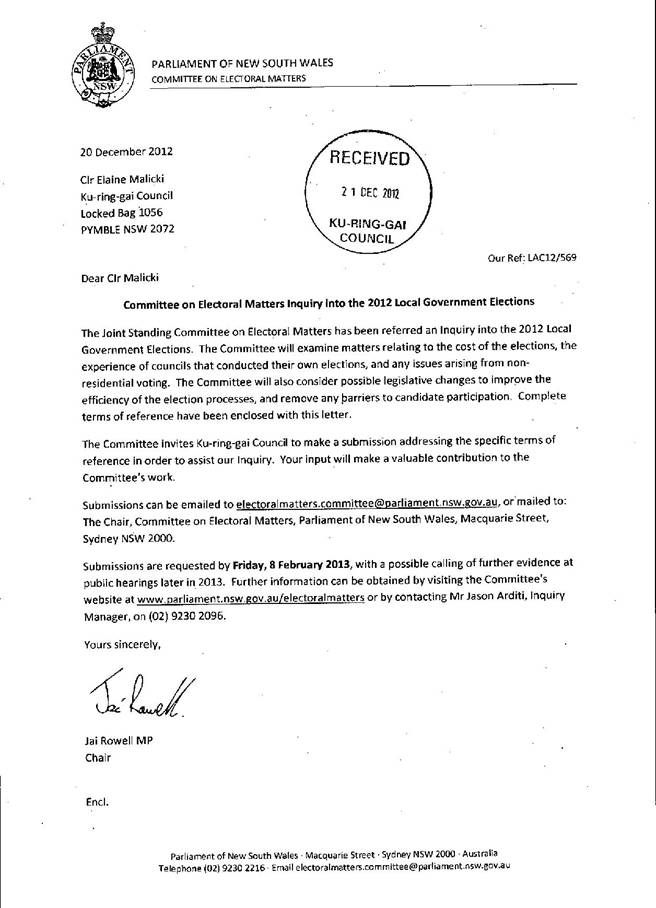

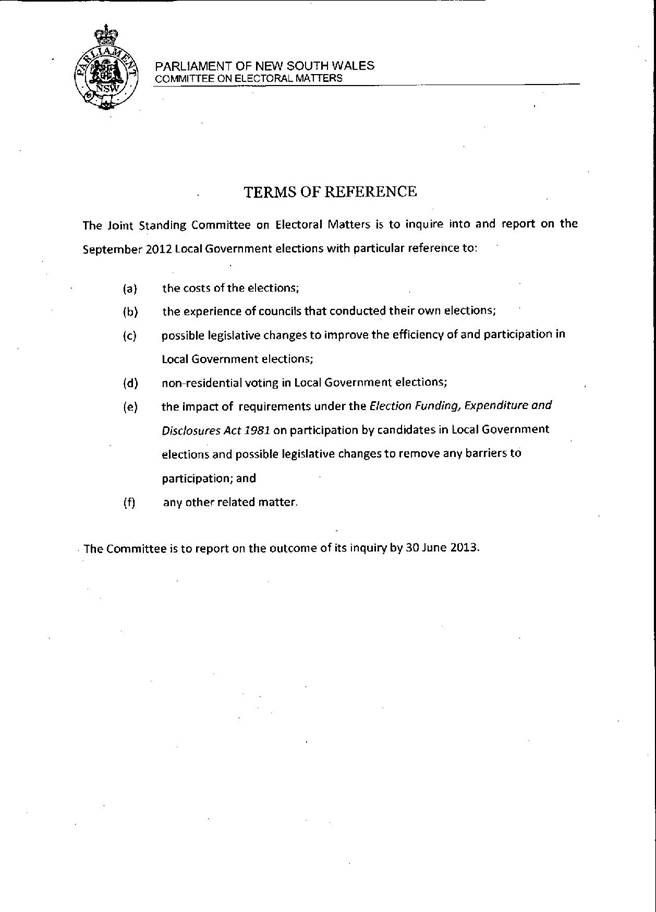

GB.5 Committee on Electoral Matters Inquiry into the 2012 Local Government Elections 297

File: S08820

To consider the comments received by Councillors in response to an invitation from the Parliament of NSW Joint Standing Committee on Electoral Matters to make a submission to the Inquiry into the 2012 Local Government Elections.

Recommendation:

That Council’s submission to the Joint Standing Committee on Electoral Matters in regards to the conduct of the 2012 local government elections include the comments contained within this report.

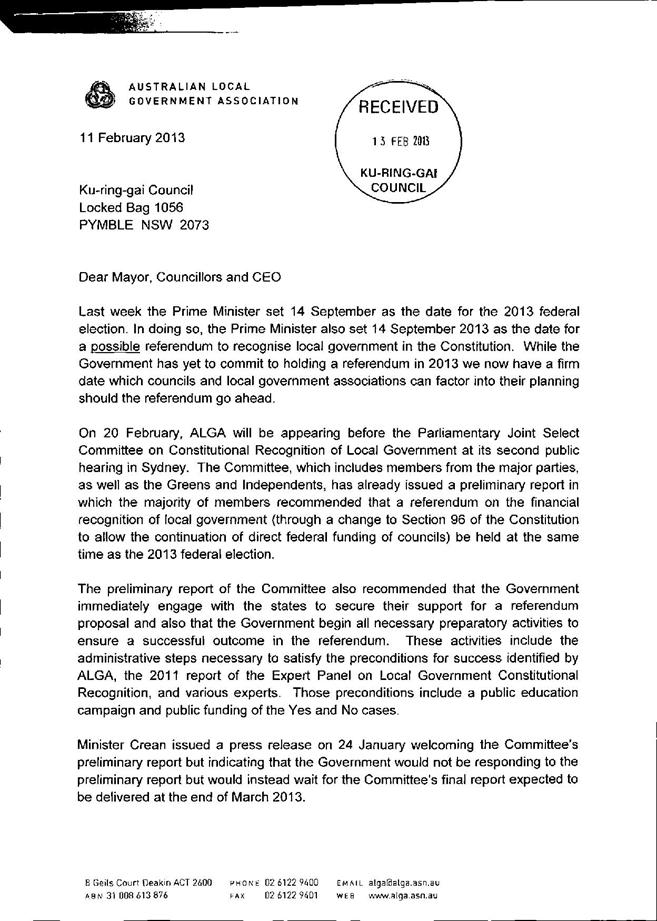

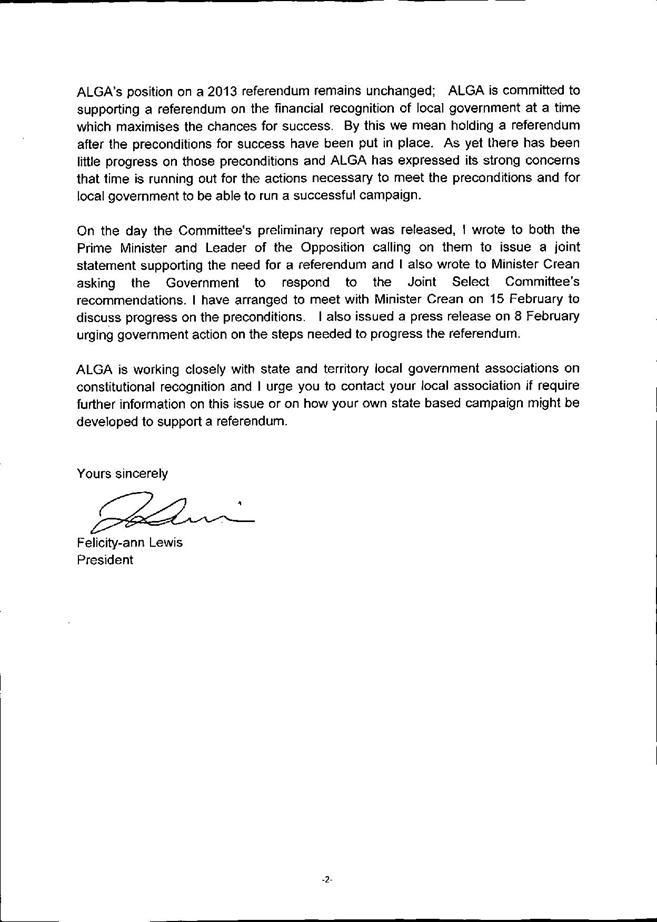

GB.6 Update on Constitutional Recognition for Local Government 313

File: S09137

To provide Councillors an update from the Australian Local Government Association in regards to the possible referendum to recognise local government in the Constitution.

Recommendation:

That council receive and note the report.

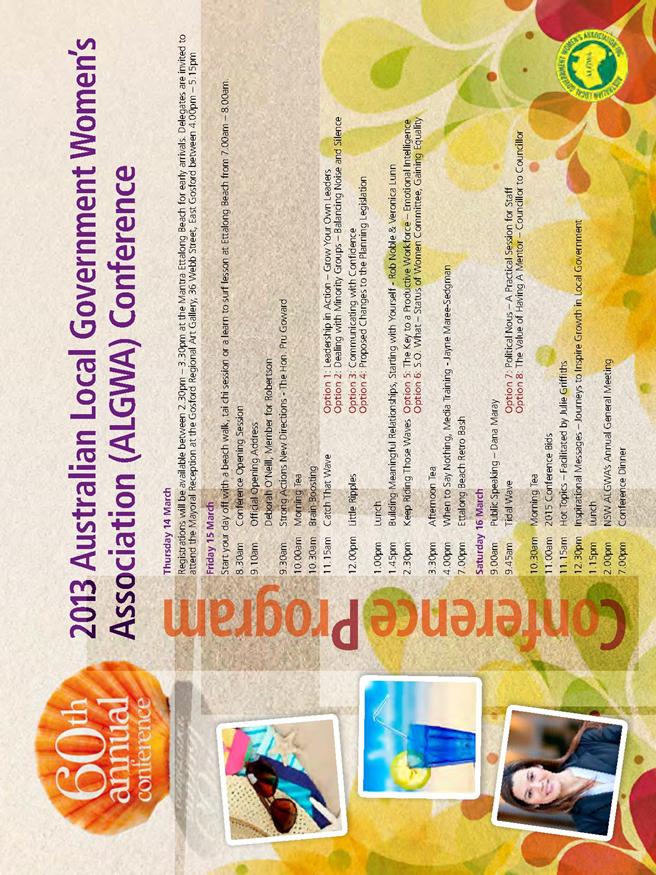

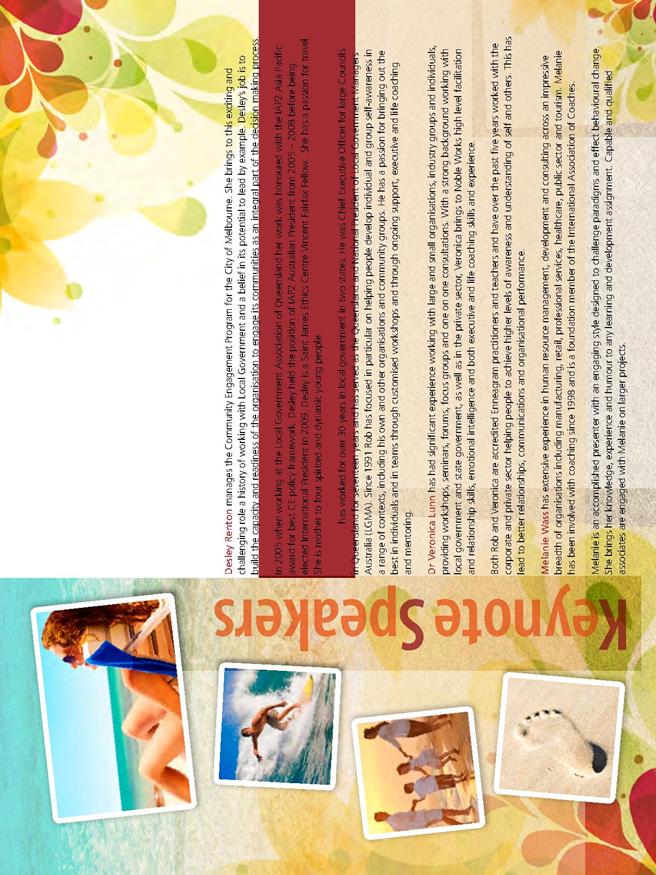

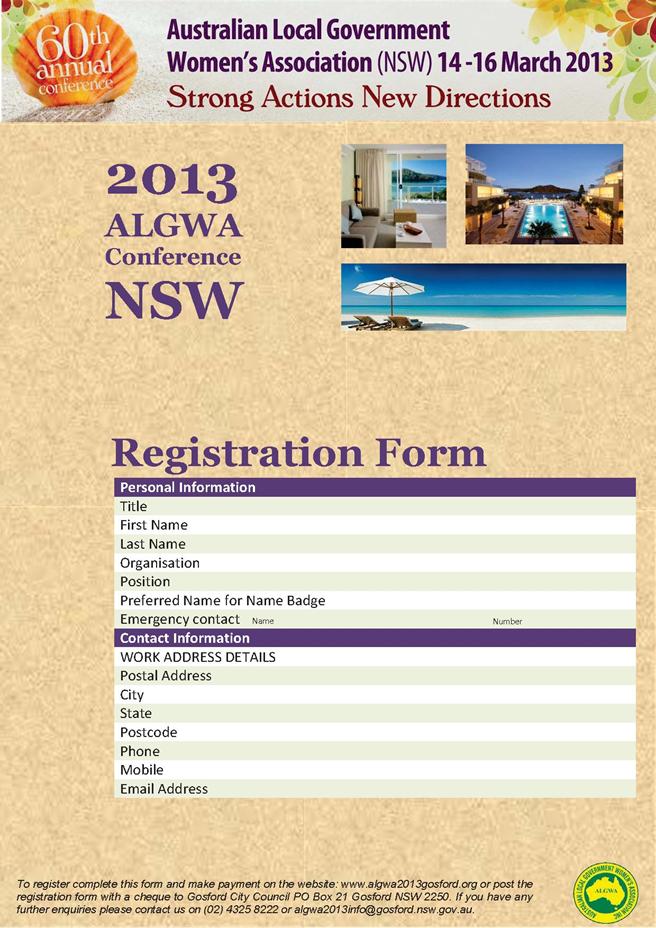

GB.7 Australian Local Government Women's Association (NSW) 59th Annual Conference March 2013 318

File: S02815

To advise Councillors of the Australian Local Government Women’s Association (NSW) Annual Conference to be held in Gosford on 14-16 March 2013.

Recommendation:

That any Councillors interested in attending the Australian Local Government Women’s Association (NSW) Annual Conference in Gosford on 14-16 March 2013 advise the General Manager by 12 noon Thursday, 28 February 2013.

GB.8 Tender T66/2012 - Investment Advisory Services 331

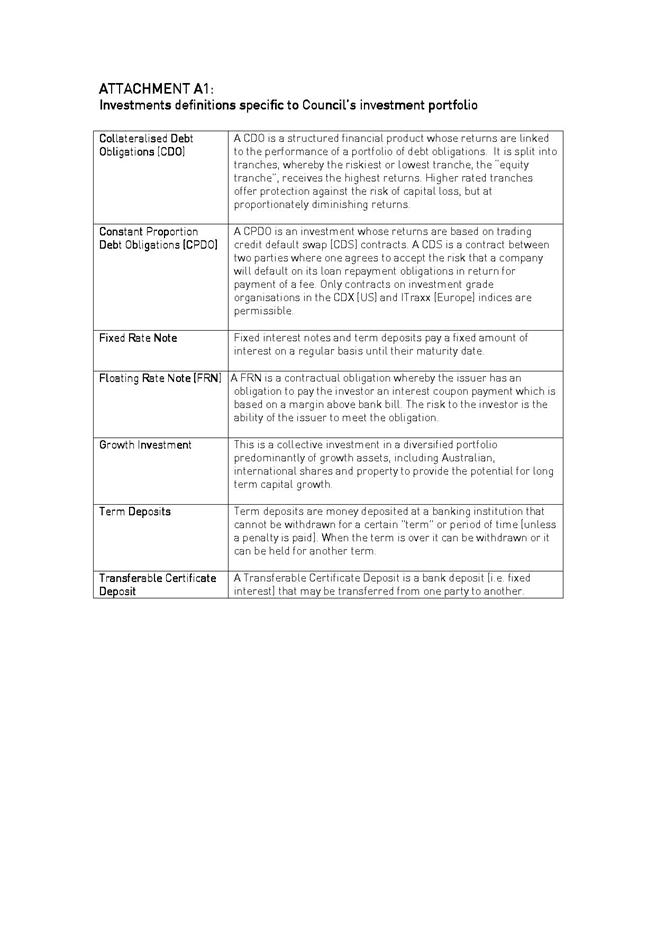

File: S05273

To report on the outcome of the Tender for provision of Investment Advisory Services.

Recommendation:

That Council accepts the Tender from Structured Credit Research & Advisory Pty Ltd to provide investment advisory services.

GB.9 Investment Report As At 31 January 2013 336

File: S05273

To present to Council investments portfolio performance for January 2013.

Recommendation:

That the summary of investments performance for January 2013 be received and noted; and that the Certificate of the Responsible Accounting Officer be noted and report adopted.

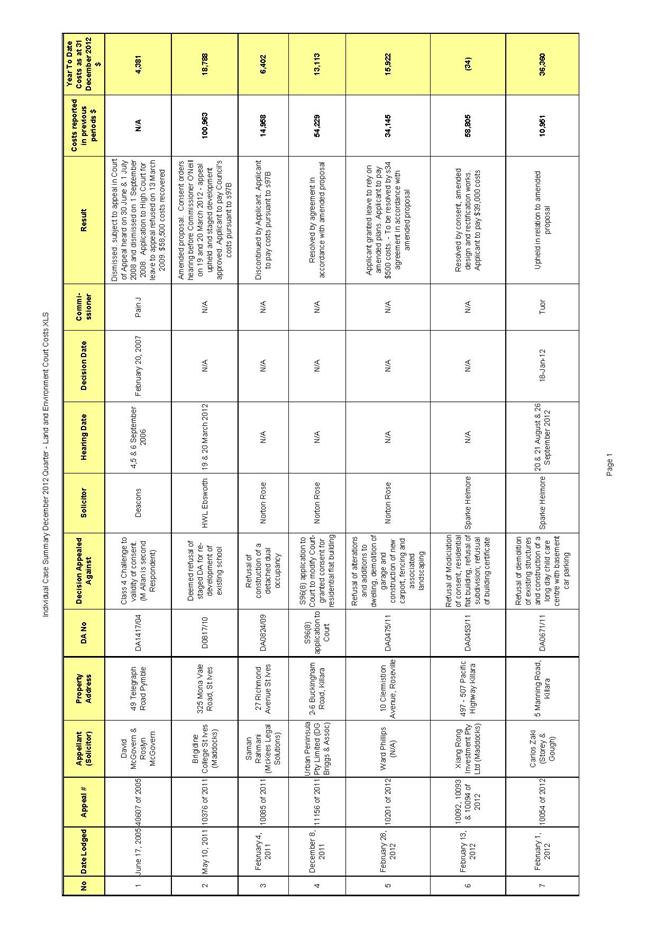

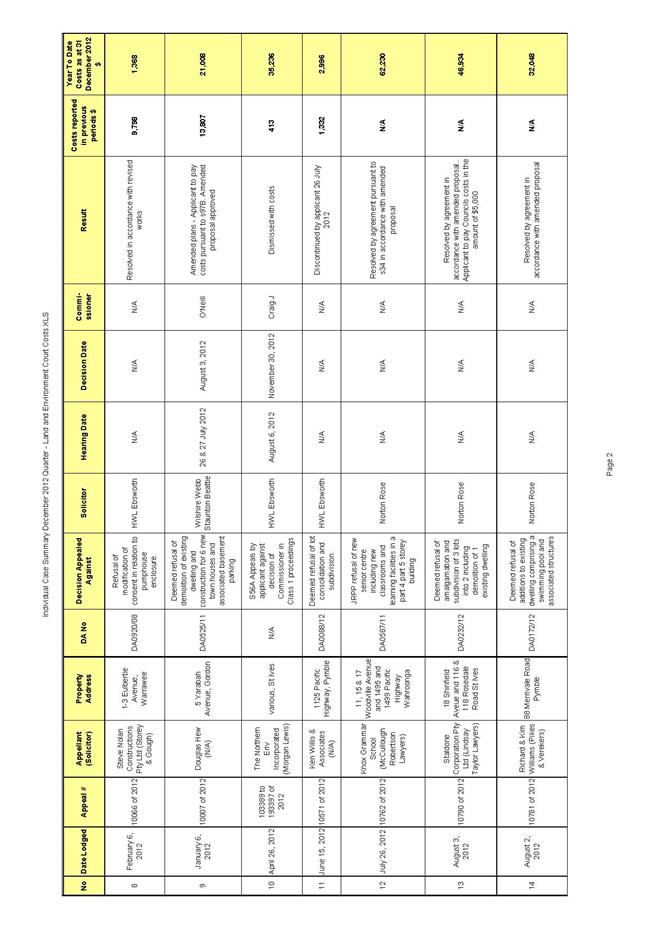

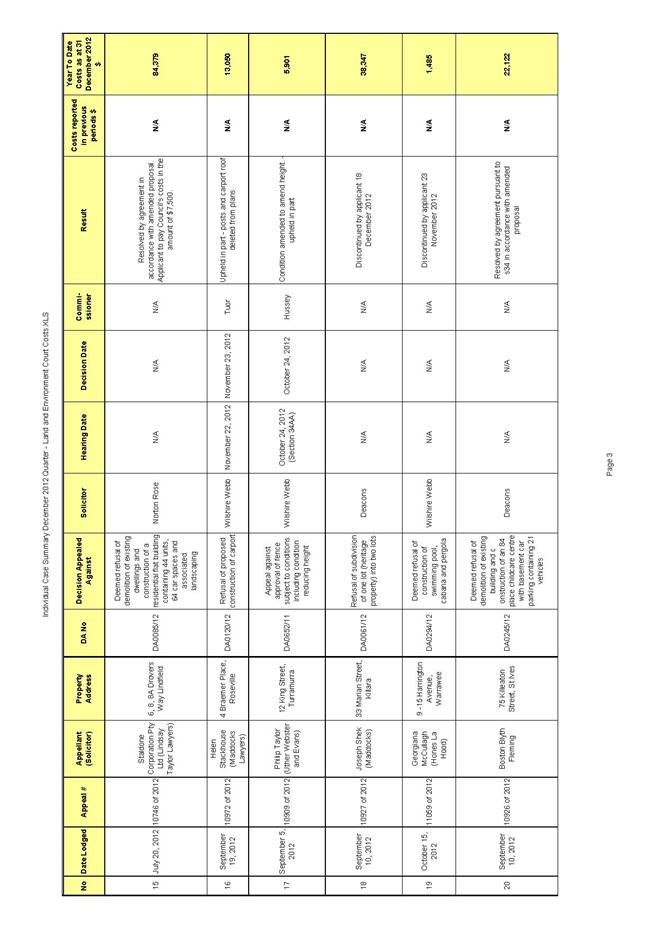

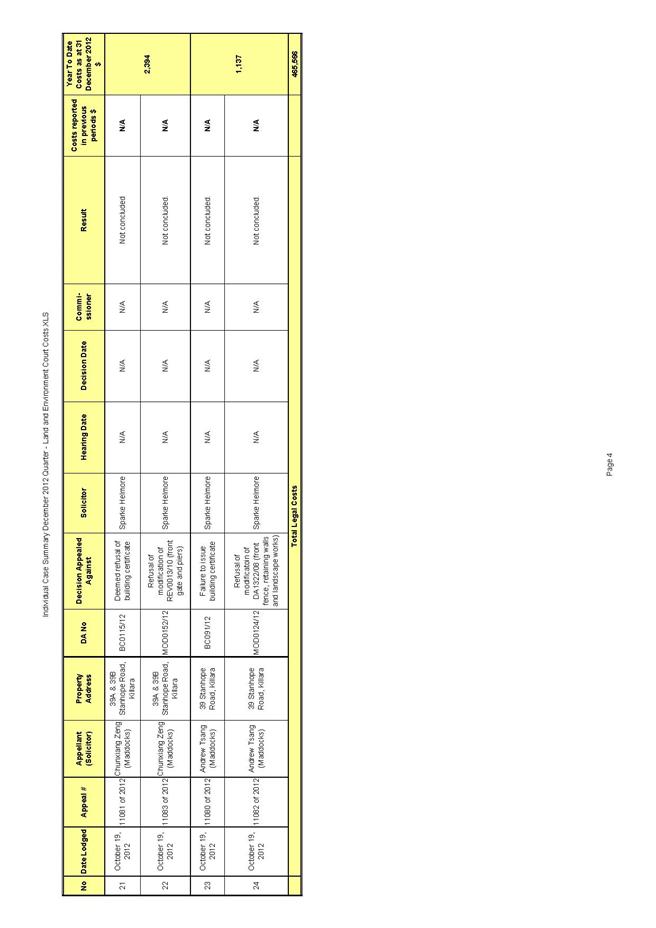

GB.10 Analysis of Land & Environment C ourt Costs - 2nd Quarter, 2012 to 2013 345

File: S05273

To report legal costs in relation to development control matters in the Land and Environment Court for the quarter ended 31 December 2012.

Recommendation:

That the analysis of Land and Environment Court costs for the six months to 31 December 2012 be received and noted.

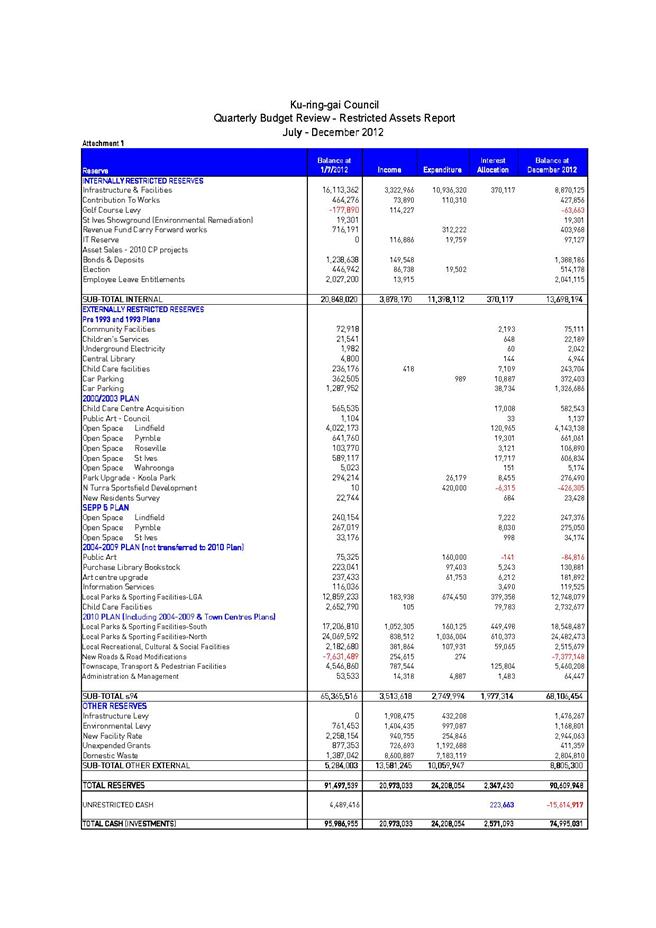

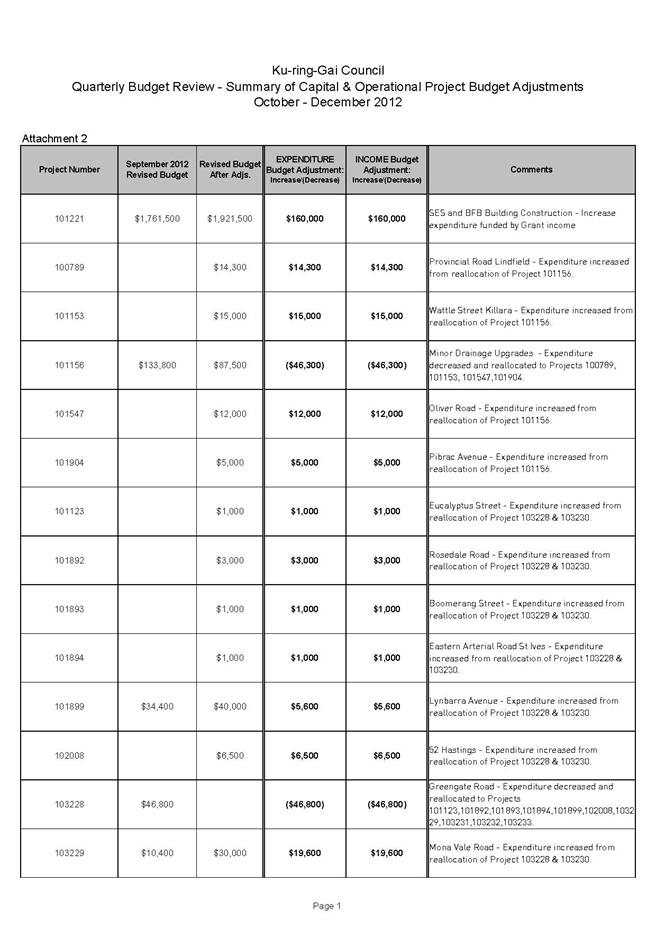

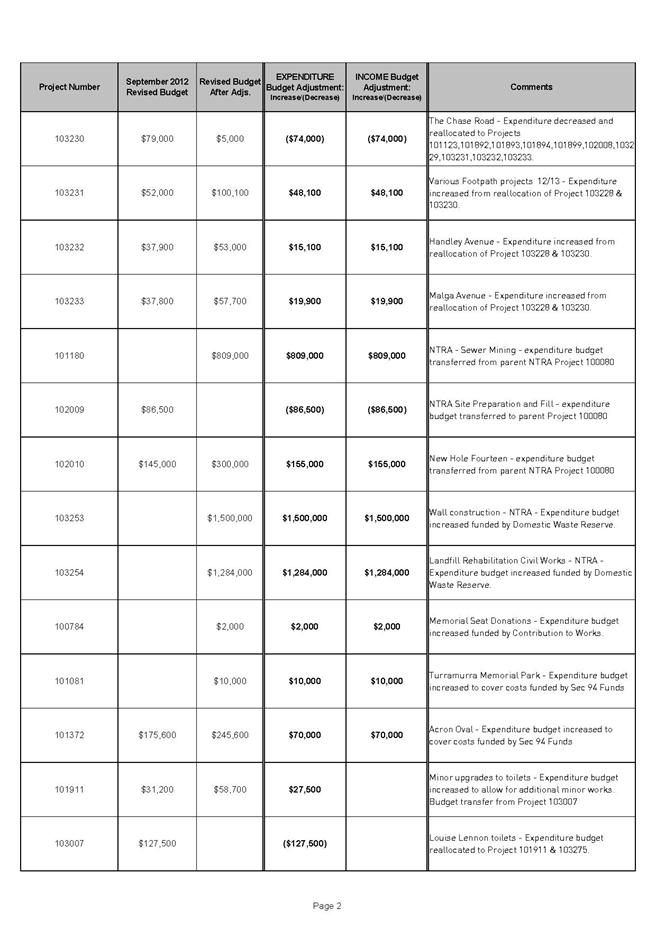

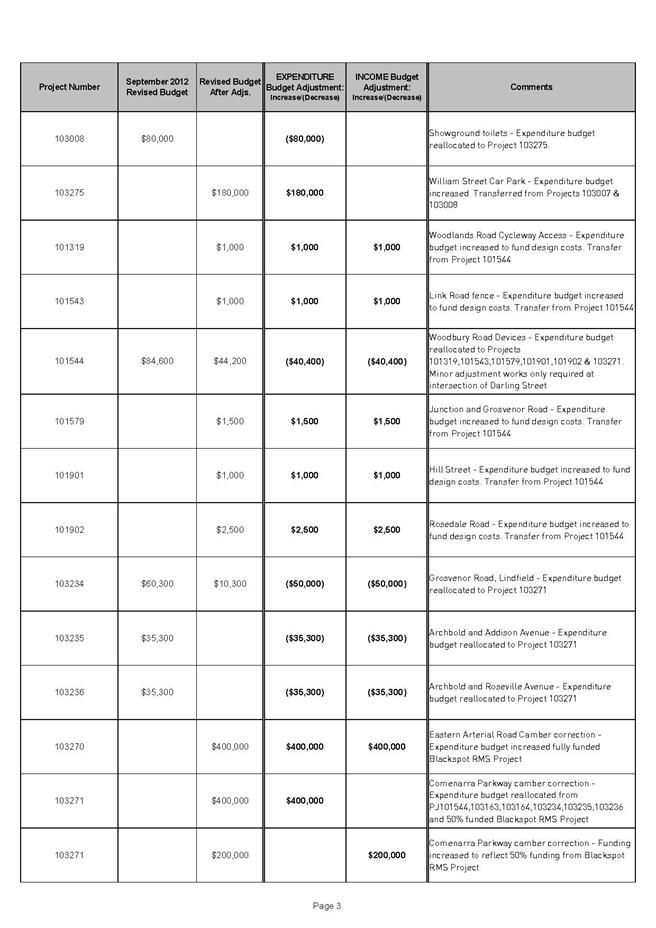

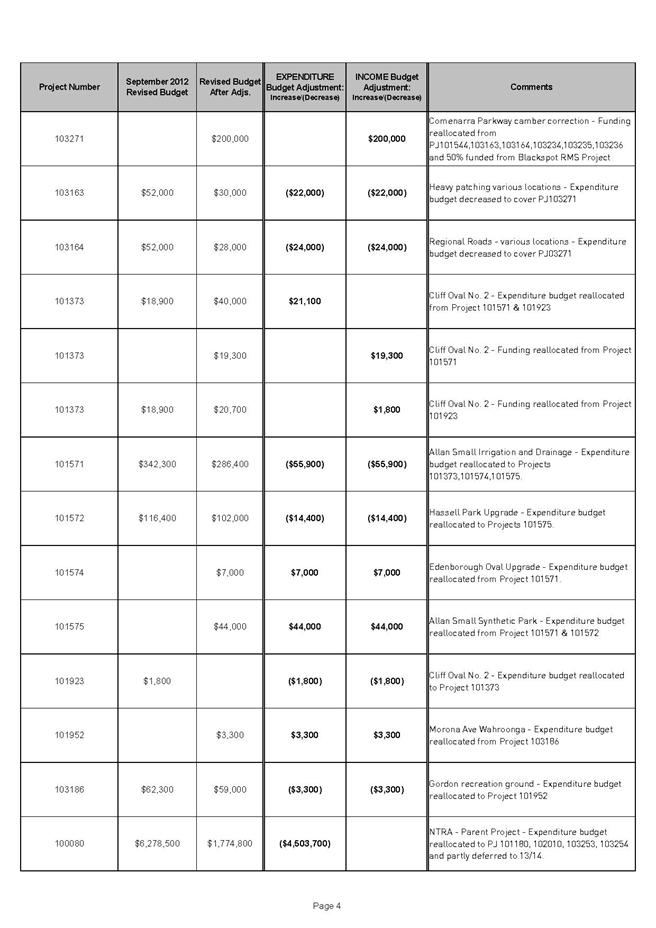

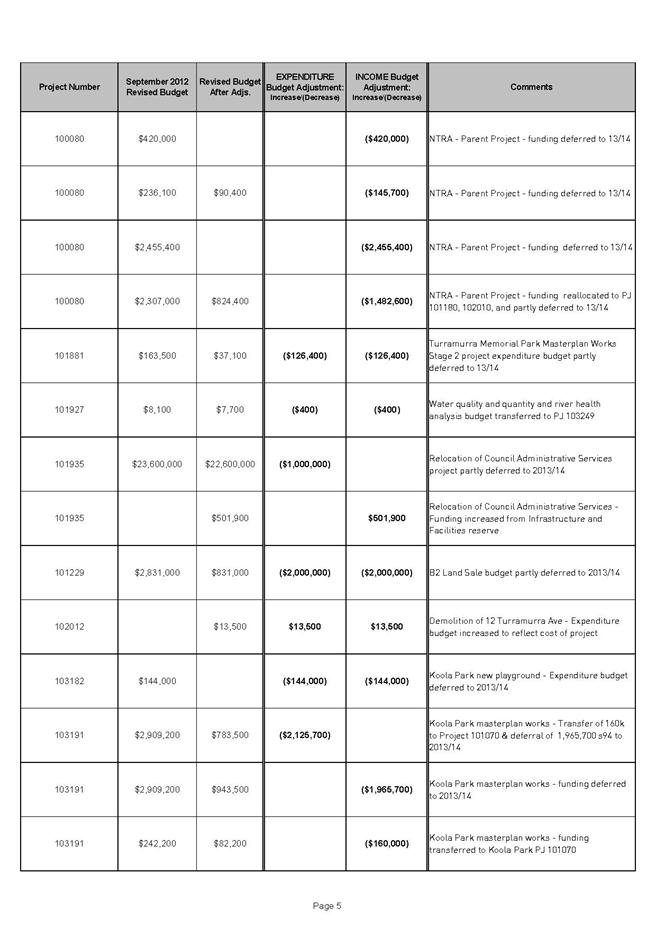

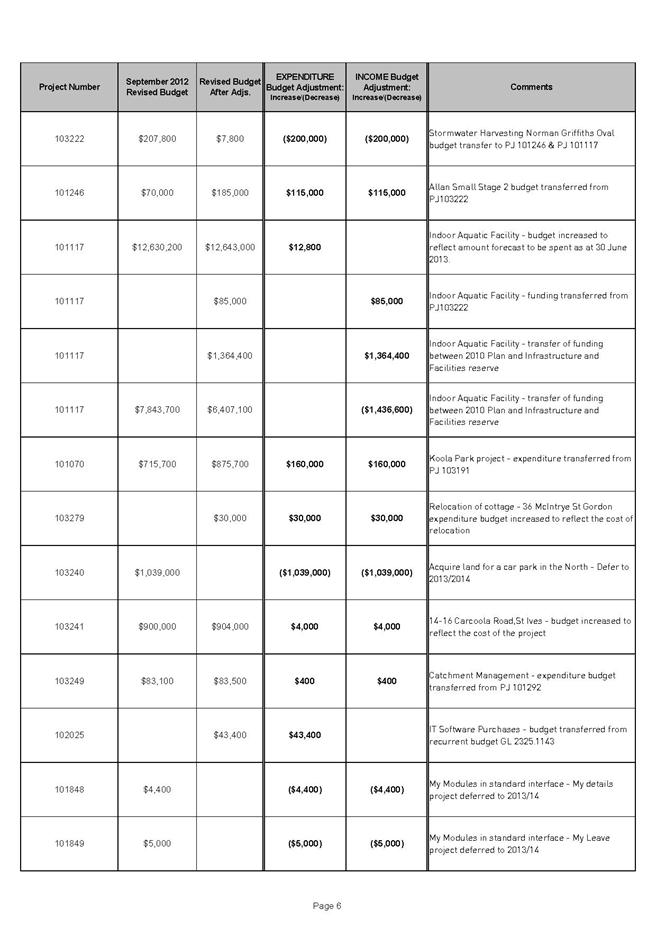

GB.11 2012 to 2013 Budget Review - 2nd Quarter ended December 2012 355

File: FY00467/2

To inform Council of the results of the second quarter budget review for 2012/13 and seek approval to adjust the annual budget based on the actual financial performance and trend for the period 1 July 2012 to 31 December 2012.

Recommendation:

That Council receive and note the December 2012 Quarterly Budget Review; and that the recommended changes to the 2012/13 Budget be adopted.

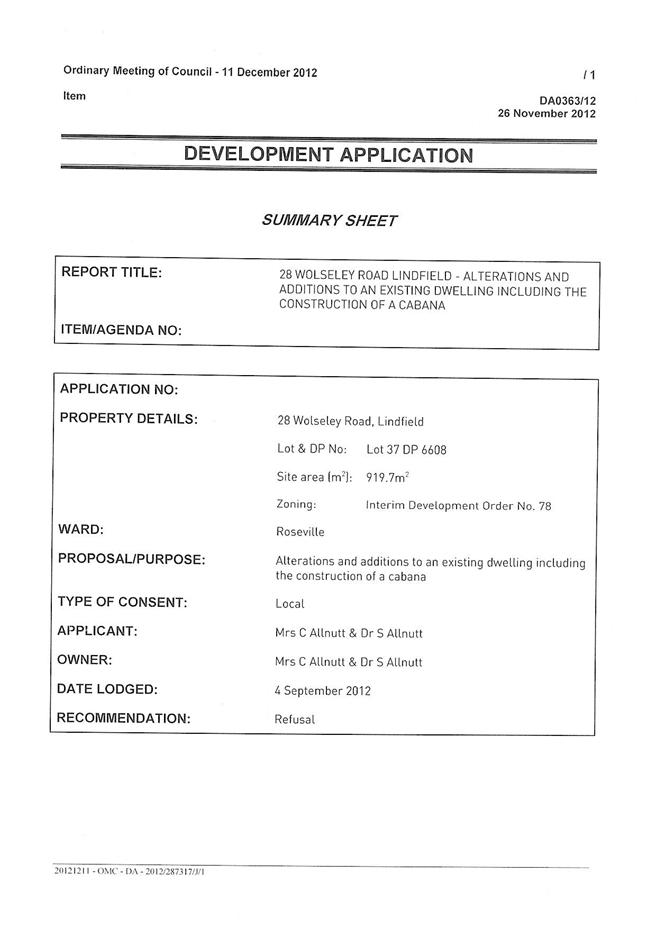

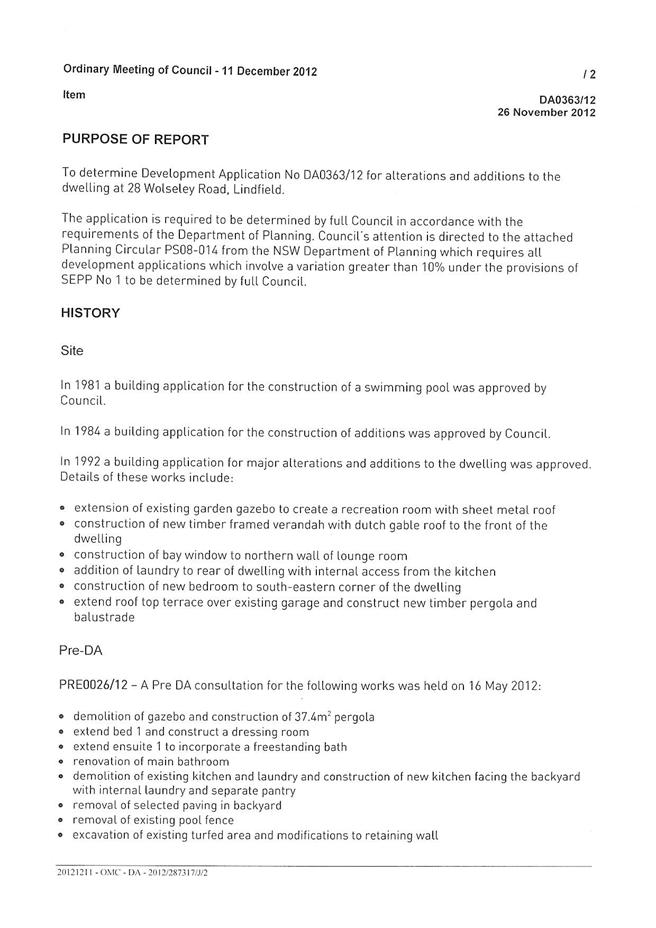

GB.12 28 Wolseley Road Lindfield - Supplementary Report 380

File: DA0363/12

To determine development application DA0363/12 for alterations and additions to an existing dwelling including the construction of a cabana.

Recommendation:

That the application be refused.

GB.13 Update Report on the Development Contributions System 402

File: S06785/2

The purpose of this report is to provide Council with an overview of key activities and highlights in the development contributions system in 2012 and anticipated highlights for 2013 and further into the future.

Recommendation:

That the information in this report be received and noted and that Council approves the divestment of 4 William Street, Turramurra.

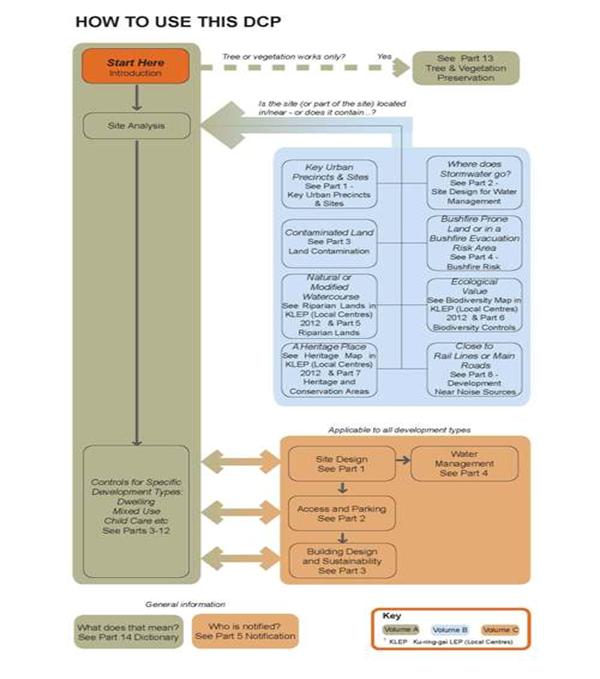

GB.14 Draft Local Centres Development Control Plan for exhibition 415

File: CY00054/5

To consider the draft of the Ku-ring-gai Local Centres Development Control Plan for public exhibition.

Recommendation:

That Council endorse the draft Ku-ring-gai (Local Centres) DCP for public exhibition.

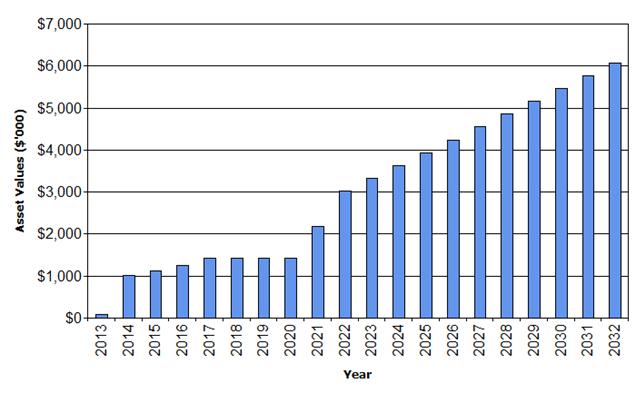

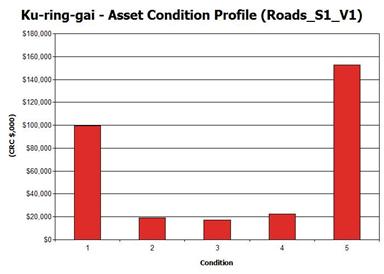

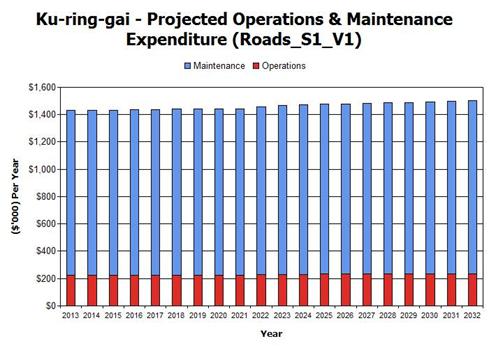

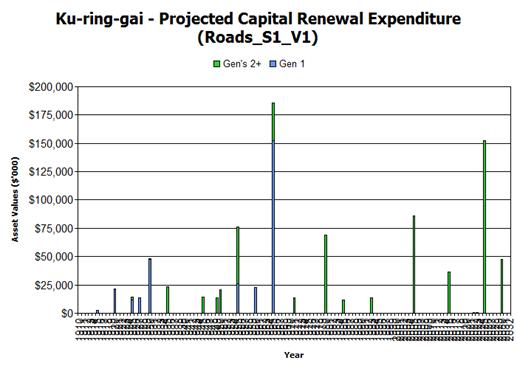

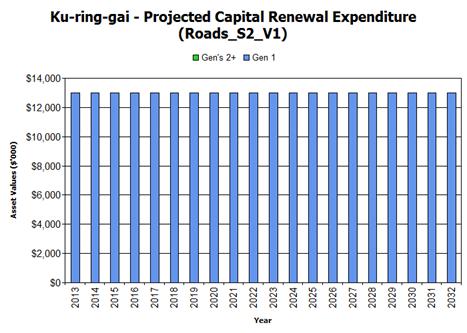

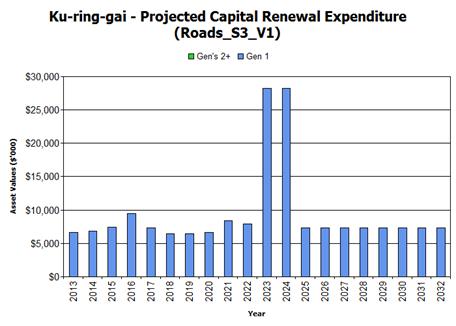

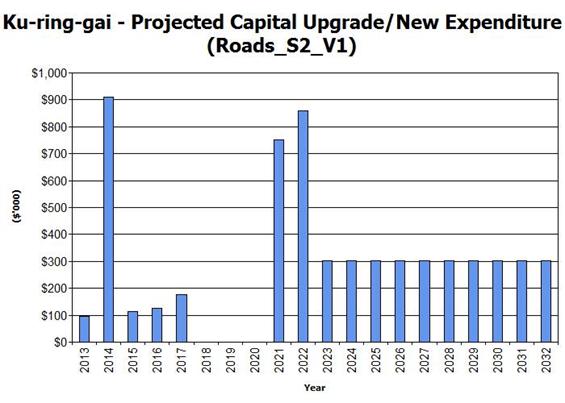

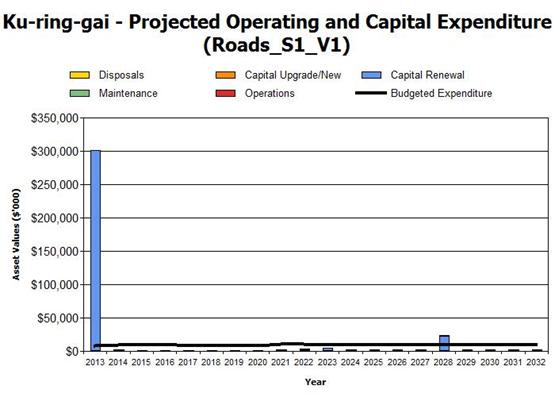

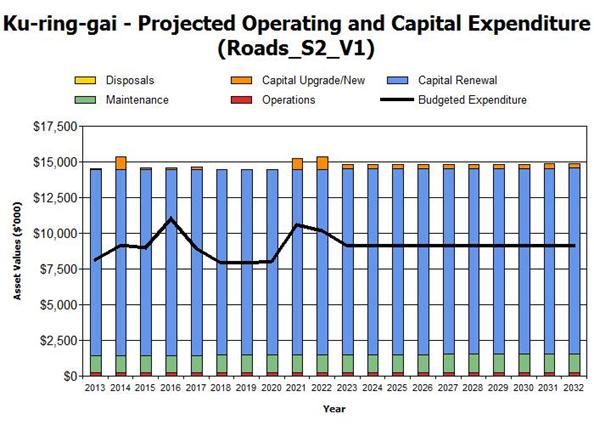

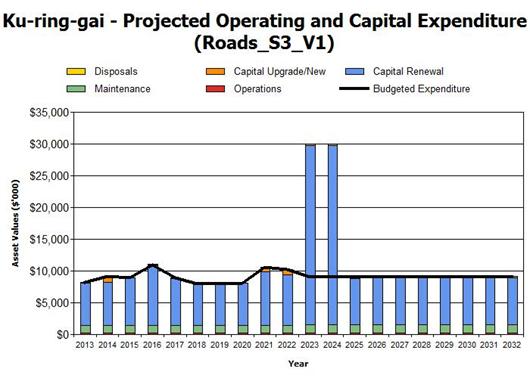

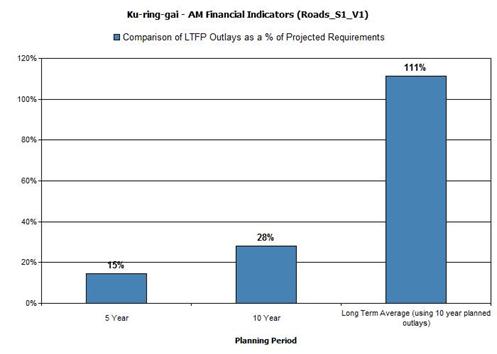

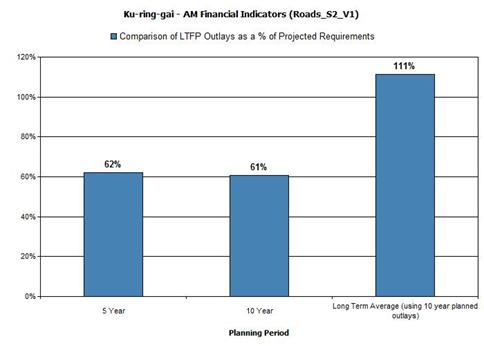

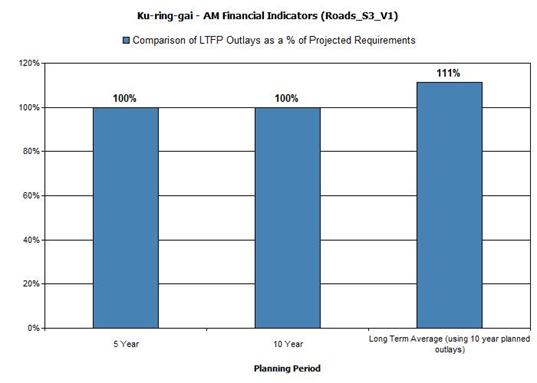

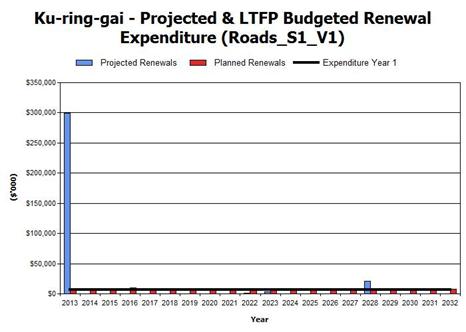

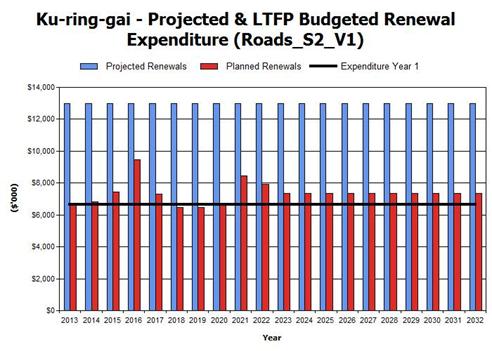

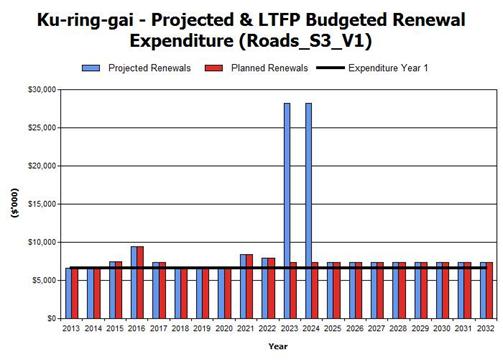

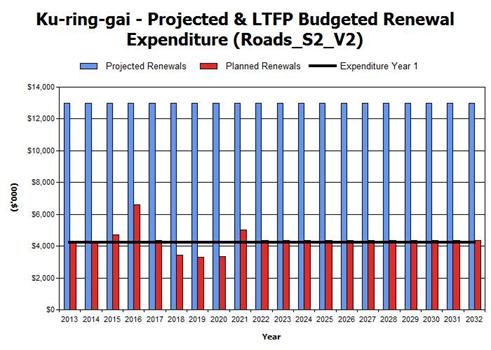

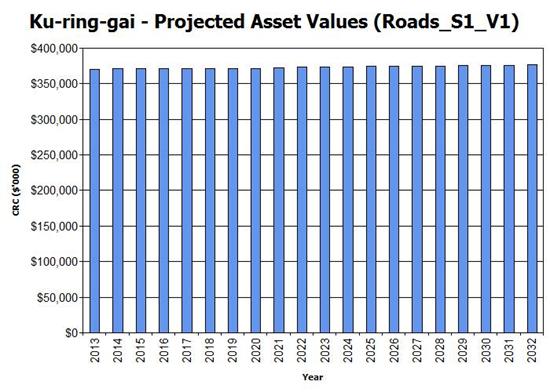

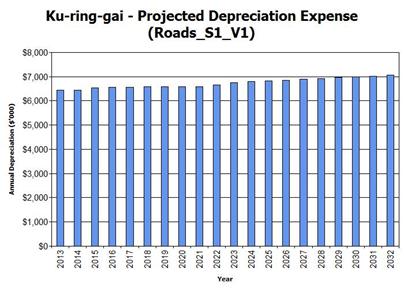

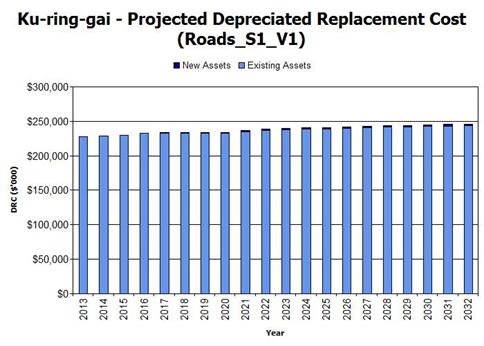

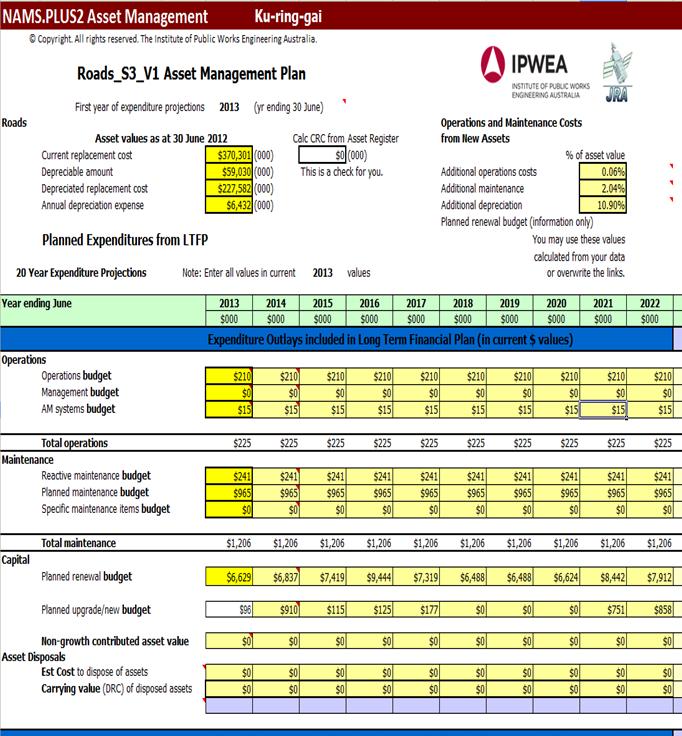

GB.15 Road Asset Management Plan 429

File: S08989

For Council to consider the revised draft Asset Management Plan for roads

Recommendation:

That Council adopt the revised Road Asset Management Plan

GB.16 Woodford Lane, Lindfield - Commuter car park 534

File: S09530

To seek the approval of Council to enter into a Project Delivery Agreement with Transport for NSW (TfNSW) for the Woodford Lane, Lindfield Commuter Car Parking Project.

Recommendation:

That Council authorise the General Manager and/or his delegate to negotiate the development of a Heads of Agreement for the Lindfield Commuter Car Parking Project and that Council authorise the General Manager to execute the legal document, to affix the Council Seal and to execute all necessary documentation, resulting from the development of the final Heads of Agreement.

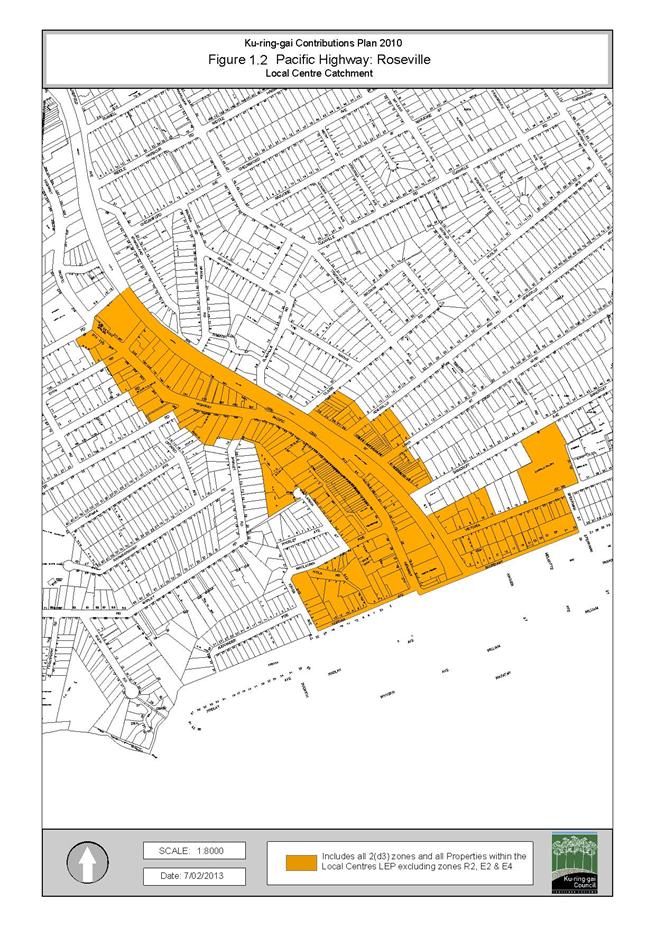

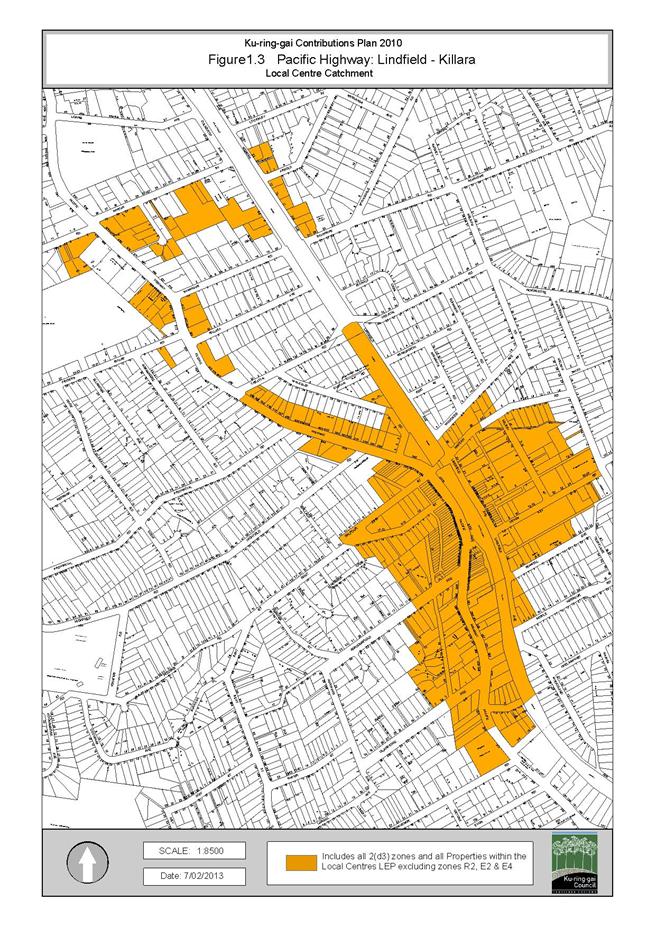

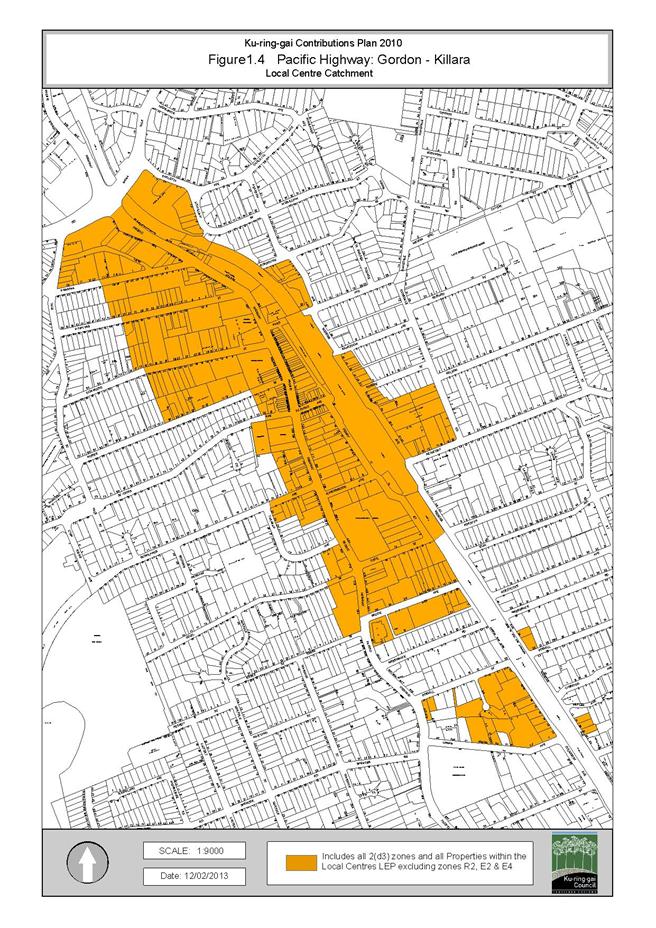

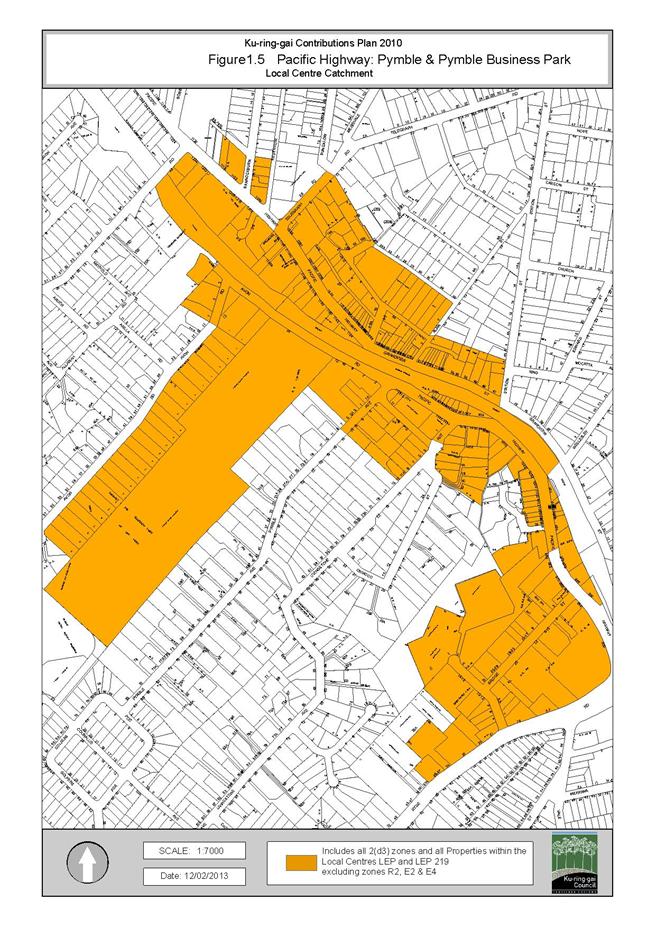

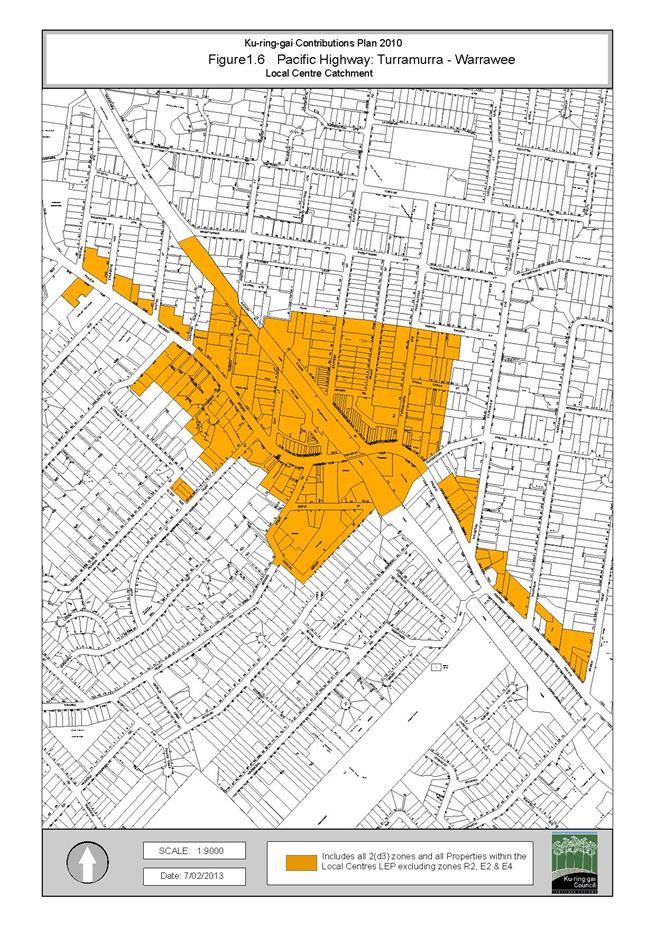

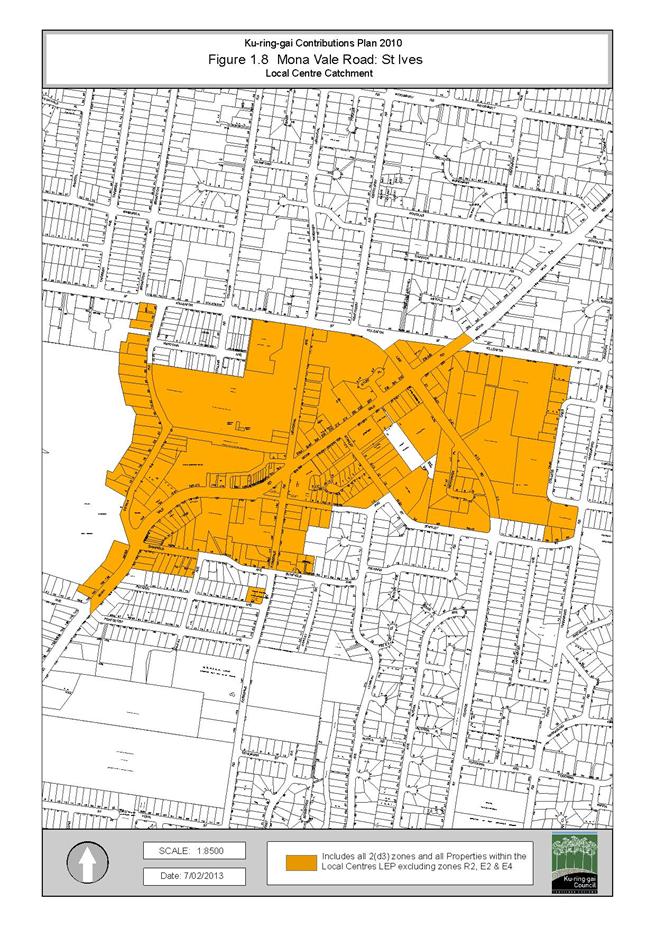

GB.17 Update to Contributions Plan Catchment Mapping to reflect Ku-ring-gai Local Environmental Plan (Local Centres) 2012 548

File: S06785/3

It is important that all Ku-ring-gai’s key planning documents operate on the same maps and catchment areas. The gazettal of Ku-ring-gai Local Environmental Plan (Local Centres) 2012 triggers the need for minor adjustments to the catchment mapping boundaries of Ku-ring-gai Contributions Plan 2010 to ensure consistency.

Recommendation:

That the amended catchment maps for Ku-ring-gai Contributions Plan 2010 be placed on public exhibition for a minimum period of 28 days.

GB.18 Proposal By Hornsby Shire Council for local Government Boundary Adjustment 560

File: S02137

To advise Council of a request from Hornsby Shire Council to enter into discussions regarding a boundary adjustment around Waratah Way and Mount Pleasant Avenue in Normanhurst, located within the Ku-ring-gai local government area.

Recommendation:

That Council notes the request from Hornsby Shire Council to enter into discussions regarding a boundary adjustment and that the General Manager write to Hornsby Shire Council to advise that Council does not wish to enter into discussions on boundary adjustments at this stage

GB.19 Tender T68/2012 - Sports Field Lighting 2013 586

File: S09536

To consider the tenders received for the supply and installation of sports field lighting at Eton Road Oval, Lindfield Oval and Golden Jubilee Sports Ground and appoint the preferred tenderer.

Recommendation:

That Council accepts the tender from Smada Electrical Services Pty Ltd for the supply and installation of sports field lighting at Eton Road Oval, Lindfield Oval and Golden Jubilee Sports Ground.

Extra Reports Circulated to Meeting

BUSINESS WITHOUT NOTICE – SUBJECT TO CLAUSE 241 OF GENERAL REGULATIONS

Questions Without Notice

Inspections Committee – SETTING OF TIME, DATE AND RENDEZVOUS

** ** ** ** ** **

MINUTES OF Ordinary Meeting of Council

HELD ON Tuesday, 5 February 2013

|

Present: |

The Mayor, Councillor E Malicki (Chairperson) (Comenarra Ward) Councillor J Pettett (Comenarra Ward) Councillors D Citer & C Szatow (Gordon Ward) Councillors C Berlioz & D Ossip (St Ives Ward) Councillors J Anderson & D Armstrong (Roseville Ward) Councillors C Fornari-Orsmond & D McDonald (Wahroonga Ward) |

|

|

|

|

Staff Present: |

General Manager (John McKee) Director Development & Regulation (Michael Miocic) Director Operations (Greg Piconi) Director Strategy & Environment (Andrew Watson) Director Community (Janice Bevan) Acting Director Corporate (John Giovinazzo) Acting Manager Finance (Angela Apostol) Manager Records & Governance (Matt Ryan) Minutes Secretary (Sigrid Banzer) |

The Meeting commenced at 7.00pm

The Mayor offered the Prayer

The Mayor adverted to the necessity for Councillors and staff to declare a Pecuniary Interest/Conflict of Interest in any item on the Business Paper.

No Interest was declared.

The following members of the public addressed Council on items not on the Agenda:

M Frost

A Powell

DOCUMENTS CIRCULATED TO COUNCILLORS

The Mayor adverted to the documents circulated in the Councillors’ papers and advised that the following matters would be dealt with at the appropriate time during the meeting:

|

e-mail Memorandum: |

Report and Attachments

Withdrawn: Refer GB.11 - Draft

Local Centres Development Control Plan for exhibition - |

|

Memorandums: |

Refer GB.8 - Draft Abandoned Shopping Trolley Policy - Memorandum by the Manager Compliance and Regulation dated 29 January 2013 with attached written submissions received.

Refer GB.11 - Draft Local Centres Development Control Plan for exhibition - Memorandum by Director Strategy and Environment dated 5 February 2013 with a revised recommendation for the Meeting item. |

|

10 |

Draft Local Centres Development Control Plan for exhibition

File: CY00054/5 Vide: GB.11

|

|

|

For Council to consider the draft of the Ku-ring-gai Local Centres Development Control Plan (Attachment 1) for public exhibition.

|

|

|

(Moved: Councillors McDonald/Anderson)

That consideration of the draft Local Centres Development Control Plan for exhibition be deferred to a Council meeting in March 2013, or earlier if possible.

CARRIED UNANIMOUSLY |

Standing Orders were suspended to deal with items

where there are speakers first after a

Motion moved by Councillors Szatow and McDonald

was CARRIED UNANIMOUSLY

|

11 |

Draft Abandoned Shopping Trolley Policy

File: S02668 Vide: GB.8

|

|

|

The following member of the public addressed Council:

R Johnson

|

|

|

To present to Council the proposed Abandoned Shopping Trolley Policy.

|

|

|

(Moved: Councillors Berlioz/Armstrong)

A. That the draft Abandoned Shopping Trolley Policy be amended as follows:

- page 160: addition of a further dot point:

“Bays should be sufficient in number to encourage easy trolley return by customers”

- page 161: addition of a further dot point:

“A map and written schedule of surveillance and collection schedules detailing abandoned trolley services around the local town centres and neighbouring residential areas is to be supplied. This service map and schedule to be reviewed and updated, at least on an annual basis. In particular, the schedule of surveillance and collection should detail the style of service to be offered and the relevant contact details of service provider. Particular attention should be given to those areas known to regularly attract abandoned trolleys, such areas are to be provided with a service at least every 24 hours.”

B. That the draft Abandoned Shopping Trolley Policy as amended above to the report be adopted by Council.

C. That Council meet with local supermarket managers, advise them of our policy to deal with abandoned shopping trolleys and seek their voluntary adoption of a suitable shopping trolley management plan that would assist in curtailing the problem.

D. That all persons who made submissions be notified of Council’s decision.

E. That Council make representations to the State Government on the matter.

F. That Council put a motion to the LGSA with regard to the handling of abandoned shopping trolleys.

CARRIED UNANIMOUSLY

The above Resolution was subject to an Amendment which was LOST. The Lost Amendment was:

(Moved: Councillors Anderson/Szatow

A. That the draft Abandoned Shopping Trolley Policy be amended as follows:

- page 160: addition of a further dot point:

“Bays should be sufficient in number to encourage easy trolley return by customers”

- page 161: addition of a further dot point:

“A map and written schedule of surveillance and collection schedules detailing abandoned trolley services around the local town centres and neighbouring residential areas is to be supplied. This service map and schedule to be reviewed and updated, at least on an annual basis. In particular, the schedule of surveillance and collection should detail the style of service to be offered and the relevant contact details of service provider. Particular attention should be given to those areas known to regularly attract abandoned trolleys, such areas are to be provided with a service at least every 24 hours.”

- addition of:

“That Council seek to provide educational information to the community to encourage the purchase of portable trolleys to own themselves”

B. That the draft Abandoned Shopping Trolley Policy as amended above to the report be adopted by Council.

C. That Council meet with local supermarket managers, advise them of our policy to deal with abandoned shopping trolleys and seek their voluntary adoption of a suitable shopping trolley management plan that would assist in curtailing the problem.

D. That all persons who made submissions be notified of Council’s decision.

E. That Council make representations to the State Government on the matter.

F. That Council put a motion to the LGSA with regard to the handling of abandoned shopping trolleys.

|

|

12 |

Committee on Electoral Matters Inquiry into the 2012 Local Government Elections

File: S08820 Vide: GB.4

|

|

|

To consider the invitation from the Parliament of NSW Committee on Electoral Matters to make a submission to the Inquiry into the 2012 Local Government Elections.

|

|

|

(Moved: Mayor, Councillors Malicki/McDonald)

A. That Council does lodge a submission to the Committee.

B. That Councillors provide any comments for possible inclusion into the submission to the General Manager by Friday, 8 February 2013.

C. That a further report containing the draft submission be referred to the Ordinary Meeting of Council to be held on the 26 February 2013 for endorsement by Council before being referred to the Committee.

CARRIED UNANIMOUSLY

The above Resolution was subject to a Motion which was LOST. The Lost Motion was:

(Moved: Councillors Anderson/Ossip

A. That Council make a submission to the Committee.

B. That Councillors provide any comments for possible inclusion into the submission to the General Manager by Friday, 8 February 2012.

C. That Council also endeavours to contact other candidates for the election and recently retired Councillors so that they may have some input.

D. That a further report containing the draft submission be referred to the Ordinary Meeting of Council to be held on the 26 February 2013 for endorsement by Council before being referred to the Committee.

|

|

13 |

Review of Financial Assistance Grants - Request for Contribution of Funds

File: S06748/3 Vide: GB.6

|

|

|

To consider the request from Sutherland Shire Council to a number of Councils for a financial contribution to engage expertise by the way of a consultant to prepare a submission on behalf of the involved Councils to the review of Financial Assistance Grants (FAGs) being held by the Commonwealth Grants Commission.

|

|

|

(Moved: Councillors Szatow/Berlioz)

That Council contribute to this request for financial support from Sutherland Shire Council to engage the services of a consultant to prepare a submission to the Commission on the review of Financial Assistance Grants.

CARRIED UNANIMOUSLY |

|

14 |

9 Wonga Wonga Street Turramurra - Demolish Existing Dwelling and Construct a Development containing 10 Self Care Apartments over Basement Parking - SEPP (Housing for Seniors or People with A Disability) 2004

File: DA0385/12 Vide: GB.10

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

Demolish existing dwelling and construct a development containing 10 self care apartments over basement parking – SEPP (Housing for Seniors or People with A Disability) 2004.

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

(Moved: Councillors Anderson/Councillor McDonald)

PURSUANT TO SECTION 80(1) OF THE ENVIRONMENTAL PLANNING AND ASSESSMENT ACT, 1979

THAT the Council, as the consent authority, grant development consent to DA0385/12 for demolition of an existing dwelling and associated structures and construction of a development comprising 10 self care apartments over basement parking pursuant to SEPP (Housing for Seniors or People with a Disability) 2004 on land at 9 Wonga Wonga Street, Turramurra, for a period of two (2) years from the date of the Notice of Determination, subject to the following conditions:

Conditions that identify approved plans:

1. Approved architectural plans and documentation (new development)

The development must be carried out in accordance with the following plans and documentation listed below and endorsed with Council’s stamp, except where amended by other conditions of this consent:

Reason: To ensure that the development is in accordance with the determination.

2. Inconsistency between documents

In the event of any inconsistency between conditions of this consent and the drawings/documents referred to above, the conditions of this consent prevail.

Reason: To ensure that the development is in accordance with the determination.

Conditions to be satisfied prior to demolition, excavation or construction:

3. Road opening permit

The opening of any footway, roadway, road shoulder or any part of the road reserve shall not be carried out without a road opening permit being obtained from Council (upon payment of the required fee) beforehand.

Reason: Statutory requirement (Roads Act 1993 Section 138) and to maintain the integrity of Council’s infrastructure.

4. Notice of commencement

At least 48 hours prior to the commencement of any development (including demolition, excavation, shoring or underpinning works), a notice of commencement of building or subdivision work form and appointment of the principal certifying authority form shall be submitted to Council.

Reason: Statutory requirement.

5. Notification of builder’s details

Prior to the commencement of any development or excavation works, the Principal Certifying Authority shall be notified in writing of the name and contractor licence number of the owner/builder intending to carry out the approved works.

Reason: Statutory requirement.

6. Dilapidation survey and report (public infrastructure)

Prior to the commencement of any development or excavation works on site, the Principal Certifying Authority shall be satisfied that a dilapidation report on the visible and structural condition of all structures of the following public infrastructure, has been completed and submitted to Council:

Public infrastructure

· Full road pavement width, including kerb and gutter, of Wonga Wonga Street over the site frontage, including the full intersection. · All driveway crossings and laybacks opposite the subject site.

The report must be completed by a consulting structural/civil engineer. Particular attention must be paid to accurately recording (both written and photographic) existing damaged areas on the aforementioned infrastructure so that Council is fully informed when assessing any damage to public infrastructure caused as a result of the development.

The developer may be held liable to any recent damage to public infrastructure in the vicinity of the site, where such damage is not accurately recorded by the requirements of this condition prior to the commencement of works.

Note: A written acknowledgment from Council must be obtained (attesting to this condition being appropriately satisfied) and submitted to the Principal Certifying Authority prior to the commencement of any excavation works.

Reason: To record the structural condition of public infrastructure before works commence.

7. Photographic archival recording

The existing house, the site and its streetscape context and relationship to adjoining properties shall be photographically recorded.

Reason: To ensure the proper management of historical artefacts to ensure their preservation.

8. Dilapidation survey and report (private property)

Prior to the commencement of any demolition or excavation works on site, the Principal Certifying Authority shall be satisfied that a dilapidation report on the visible and structural condition of all structures upon the following lands, has been completed and submitted to Council:

The dilapidation report must include a photographic survey of adjoining properties detailing their physical condition, both internally and externally, including such items as walls ceilings, roof and structural members. The report must be completed by a consulting structural/geotechnical engineer as determined necessary by that professional based on the excavations for the proposal and the recommendations of the submitted geotechnical report.

In the event that access for undertaking the dilapidation survey is denied by a property owner, the applicant must demonstrate in writing to the satisfaction of the Principal Certifying Authority that all reasonable steps have been taken to obtain access and advise the affected property owner of the reason for the survey and that these steps have failed.

Note: A copy of the dilapidation report is to be provided to Council prior to any excavation works been undertaken. The dilapidation report is for record keeping purposes only and may be used by an applicant or affected property owner to assist in any civil action required to resolve any dispute over damage to adjoining properties arising from works.

Reason: To record the structural condition of likely affected properties before works commence.

9. Construction and traffic management plan

The applicant must submit to Council a Construction Traffic Management Plan (TMP), which is to be approved prior to the commencement of any works on site.

The plan is to consist of a report with Traffic Control Plans attached.

The report is to contain commitments which must be followed by the demolition and excavation contractor, builder, owner and subcontractors. The TMP applies to all persons associated with demolition, excavation and construction of the development.

The report is to contain construction vehicle routes for approach and departure to and from all directions.

The report is to contain a site plan showing entry and exit points. Swept paths are to be shown on the site plan showing access and egress for an 11 metre long heavy rigid vehicle.

The Traffic Control Plans are to be prepared by a qualified person (red card holder). One must be provided for each of the following stages of the works:

· Demolition · Excavation · Concrete pour · Construction of vehicular crossing and reinstatement of footpath · Traffic control for vehicles reversing into or out of the site.

Traffic controllers must be in place at the site entry and exit points to control heavy vehicle movements in order to maintain the safety of pedestrians and other road users.

When a satisfactory TMP is received, a letter of approval will be issued with conditions attached. Traffic management at the site must comply with the approved TMP as well as any conditions in the letter issued by Council. Council’s Rangers will be patrolling the site regularly and fines will be issued for any non-compliance with this condition.

Reason: To ensure that appropriate measures have been considered during all phases of the construction process in a manner that maintains the environmental amenity and ensures the ongoing safety and protection of people.

10. Work zone

A works zone shall be provided along the site frontage. The applicant must make a written application to the Ku-ring-gai Local Traffic Committee to install the work zone. Work zones are provided specifically for the set down and pick up of materials and not for the parking of private vehicles associated with the site. Work zones will generally not be approved where there is sufficient space on-site for the setting down and picking up of goods being taken to or from a construction site.

If the work zone is approved by the Local Traffic Committee, the applicant must obtain a written copy of the related resolution from the Ku-ring-gai Local Traffic Committee and submit this to the Principal Certifying Authority prior to commencement of any works on site.

Where approval of the work zone is resolved by the Committee, the necessary work zone signage shall be installed (at the cost of the applicant) and the adopted fee paid prior to commencement of any works on site. At the expiration of the work zone approval, the applicant is required to remove the work zone signs and reinstate any previous signs at their expense.

In the event the work zone is required for a period beyond that initially approved by the Traffic Committee, the applicant shall make a payment to Council for the extended period in accordance with Council’s schedule of fees and charges for work zones prior to the extended period commencing.

Reason: To ensure that appropriate measures have been made for the operation of the site during the construction phase.

11. Sediment controls

Prior to any work commencing on site, sediment and erosion control measures shall be installed along the contour immediately downslope of any future disturbed areas.

The form of the sediment controls to be installed on the site shall be determined by reference to the ‘NSW Department of Housing manual ‘Managing Urban Stormwater: Soils and Construction’. The erosion controls shall be maintained in an operational condition until the development activities have been completed and the site fully stabilised. Sediment shall be removed from the sediment controls following each heavy or prolonged rainfall period.

Reason: To preserve and enhance the natural environment.

12. Erosion and drainage management

Earthworks and/or demolition of any existing buildings shall not commence until an erosion and sediment control plan is submitted to and approved by the Principal Certifying Authority. The plan shall comply with the guidelines set out in the NSW Department of Housing manual "Managing Urban Stormwater: Soils and Construction" certificate. Erosion and sediment control works shall be implemented in accordance with the erosion and sediment control plan.

Reason: To preserve and enhance the natural environment.

13. Tree protection fencing

To preserve the following tree/s, no work shall commence until the area beneath their canopy is fenced off at the specified radius from the trunk/s to prevent any activities, storage or the disposal of materials within the fenced area. The fence/s shall be maintained intact until the completion of all demolition/building work on site.

Reason: To protect existing trees during the construction phase.

14. Tree protection fencing excluding structure

To preserve the following tree/s, no work shall commence until the area beneath their canopy excluding that area of the approved (existing driveway or basement to Block B) shall be fenced off for the specified radius from the trunk to prevent any activities, storage or the disposal of materials within the fenced area. The fence/s shall be maintained intact until the completion of all demolition/building work on site:

Reason: To protect existing trees during the construction phase.

15. Tree protective fencing type galvanised mesh

The tree protection fencing shall be constructed of galvanised pipe at 2.4 metre spacing and connected by securely attached chain mesh fencing to a minimum height of 1.8 metres in height prior to work commencing.

Reason: To protect existing trees during construction phase.

16. Tree protection signage

Prior to works commencing, tree protection signage is to be attached to each tree protection zone, displayed in a prominent position and the sign repeated at 10 metres intervals or closer where the fence changes direction. Each sign shall contain in a clearly legible form, the following information:

Tree protection zone.

· This fence has been installed to prevent damage to the trees and their growing environment both above and below ground and access is restricted. · Any encroachment not previously approved within the tree protection zone shall be the subject of an arborist's report. · The arborist's report shall provide proof that no other alternative is available. · The Arborist's report shall be submitted to the Principal Certifying Authority for further consultation with Council. · The name, address, and telephone number of the developer.

Reason: To protect existing trees during the construction phase.

17. Ground protection – avoiding soil compaction

To preserve the following tree/s and avoid soil compaction, no work shall commence until temporary measures to avoid soil compaction (eg rumble boards) beneath the canopy of the following tree/s is/are installed:

Reason: To protect existing trees during the construction phase.

18. Tree fencing inspection

Upon installation of the required tree protection measures, an inspection of the site by the Principal Certifying Authority is required to verify that tree protection measures comply with all relevant conditions.

Reason: To protect existing trees during the construction phase.

Conditions to be satisfied prior to the issue of the construction certificate:

19. Amendments to approved landscape plans

Prior to the issue of a Construction Certificate, the Principal Certifying Authority shall be satisfied that the approved landscape plans, listed below and endorsed with Council’s stamp, have been amended in accordance with the requirements of this condition as well as other conditions of this consent:

The following changes are required to the Landscape Plan:

1. To reduce the bulk of the new building, three (3) additional small ornamental trees, such as Lagerstroemia indica (Crepe Myrtle) or similar, shall be shown planted in the eastern boundary planting bed, evenly spaced along the eastern elevation of Building A.

Prior to the issue of the Construction Certificate, the Principal Certifying Authority shall be satisfied that the landscape plan has been amended are required by this condition.

Note: An amended plan, prepared by a landscape architect or qualified landscape designer shall be submitted to the Certifying Authority.

Reason: To ensure adequate landscaping of the site.

20. Removal of existing tennis court fencing

All fencing associated with the existing tennis court is to be removed.

Reason: The proposal involves the removal of the tennis court, accordingly no further purpose is served in retaining the tennis court fencing.

21. Amendments to approved environmental site management plan

Prior to the issue of a Construction Certificate, the Principal Certifying Authority shall be satisfied that the approved environmental site management plan, listed below and endorsed with Council’s stamp, have been amended in accordance with the requirements of this condition as well as other conditions of this consent:

The following changes are required to the environmental site management plan:

1) Tree protection fencing location to be amended in accordance with conditions of consent

2) All notes regarding tree protection measures, including location and type of fencing or ground protection, shall be amended or deleted in accordance with the conditions of consent.

3) All proposed stockpiles and site sheds are to be shown located outside the tree protection zone of trees to be retained.

Prior to the issue of the Construction Certificate, the Principal Certifying Authority shall be satisfied that the environmental site management plan has been amended as required by this condition.

Reason: To ensure the protection of trees.

22. Long service levy

In accordance with Section 109F(i) of the Environmental Planning and Assessment Act a Construction Certificate shall not be issued until any long service levy payable under Section 34 of the Building and Construction Industry Long Service Payments Act 1986 (or where such levy is payable by instalments, the first instalment of the levy) has been paid. Council is authorised to accept payment. Where payment has been made elsewhere, proof of payment is to be provided to Council.

Reason: Statutory requirement.

23. Builder’s indemnity insurance

The applicant, builder, developer or person who does the work on this development, must arrange builder’s indemnity insurance and submit the certificate of insurance in accordance with the requirements of Part 6 of the Home Building Act 1989 to the Certifying Authority for endorsement of the plans accompanying the Construction Certificate.

It is the responsibility of the applicant, builder or developer to arrange the builder's indemnity insurance for residential building work over the value of $20,000. The builder's indemnity insurance does not apply to commercial or industrial building work or to residential work valued at less than $20,000, nor to work undertaken by persons holding an owner/builder's permit issued by the Department of Fair Trading (unless the owner/builder's property is sold within 7 years of the commencement of the work).

Reason: Statutory requirement.

24. Access for people with disabilities (residential)

Prior to the issue of the Construction Certificate, the Certifying Authority shall be satisfied that access for people with disabilities to and from and between the public domain, residential units and all common open space areas is provided. Consideration must be given to the means of dignified and equitable access.

Compliant access provisions for people with disabilities shall be clearly shown on the plans submitted with the Construction Certificate. All details shall be provided to the Principal Certifying Authority prior to the issue of the Construction Certificate. All details shall be prepared in consideration of the Disability Discrimination Act, and the relevant provisions of AS1428.1, AS1428.2, AS1428.4 and AS 1735.12.

Reason: To ensure the provision of equitable and dignified access for all people in accordance with disability discrimination legislation and relevant Australian Standards.

25. Stormwater management plan

Prior to issue of the Construction Certificate, the applicant must submit, for approval by the Principal Certifying Authority, scale construction plans and specifications in relation to the stormwater management and disposal system for the development. The plan(s) must be based on Stormwater Management Plans Drawing No. 1328 S1 – S4 Rev. 'E', dated 12 September 2012, prepared by John Romanous & Associates Pty Ltd and must include the following detail:

· exact location and reduced level of discharge point to the public drainage system · Layout of the property drainage system components, including but not limited to (as required) gutters, downpipes, spreaders, pits, swales, kerbs, cut-off and intercepting drainage structures, subsoil drainage, flushing facilities and all ancillary stormwater plumbing - all designed for a 235mm/hour rainfall intensity for a duration of five (5) minutes (1:50 year storm recurrence) · location(s), dimensions and specifications for the required rainwater storage and reuse tanks and systems and where proprietary products are to be used, manufacturer specifications or equivalent shall be provided · specifications for reticulated pumping facilities (including pump type and manufacturer specifications) and ancillary plumbing to fully utilise rainwater in accordance with Ku-ring-gai Council Development Control Plan 47 and/or BASIX commitments · details of the required on-site detention tanks required by Ku-ring-gai Water Management DCP 47, including dimensions, materials, locations, orifice and discharge control pit details as required (refer Chapter 6 and Appendices 2, 3 and 5 of DCP 47 for volume, PSD and design requirements) · the required basement stormwater pump-out system is to cater for driveway runoff and subsoil drainage (refer appendix 7.1.1 of Development Control Plan 47 for design)

The above construction drawings and specifications are to be prepared by a qualified and experienced civil/hydraulic engineer in accordance with Council’s Water Management Development Control Plan 47, Australian Standards 3500.2 and 3500.3 - Plumbing and Drainage Code and the Building Code of Australia.

Reason: To protect the environment.

26. Stormwater detention

Prior to the issue of a Construction Certificate, the Principal Certifying Authority is to be satisfied that an on-site stormwater detention system must be provided to control the rate of runoff leaving the site. The minimum volume of the required on-site detention system must be determined in accordance with Chapter 6 of the Ku-ring-gai Council Water Management Development Control Plan 47 - having regard to the specified volume concession offered in lieu of installing rainwater retention tanks. The on-site detention system must be designed by a qualified civil/hydraulic engineer and must satisfy the design controls set out in Appendix 5 of DCP 47.

Reason: To protect the environment.

27. Excavation for services

Prior to the issue of the Construction Certificate, the Principal Certifying Authority shall be satisfied that no proposed underground services (ie: water, sewerage, drainage, gas or other service) unless previously approved by conditions of consent, are located beneath the canopy of any tree protected under Council’s Tree Preservation Order, located on the subject allotment and adjoining allotments.

Note: A plan detailing the routes of these services and trees protected under the Tree Preservation Order shall be submitted to the Principal Certifying Authority.

Reason: To ensure the protection of trees.

28. Recycling and waste management

Prior to the issue of the Construction Certificate, the Certifying Authority shall be satisfied that the development provides a common garbage collection/separation area sufficient in size to store all wheelie garbage bins and recycling bins provided by Council for the number of units in the development in accordance with DCP 40. The garbage collection point is to be accessible by Council’s Waste Collection Services.

The responsibility for:

· the cleaning of waste rooms and waste service compartments; and · the transfer of bins within the property, and to the collection point once the development is in use;

shall be determined when designing the system and clearly stated in the Waste Management Plan.

Note: The architectural plans are to be amended and provided to the Certifying Authority.

Reason: Environmental protection.

29. Noise from plant in residential zone

Where any form of mechanical ventilation equipment or other noise generating plant is proposed as part of the development, prior to the issue of the Construction Certificate the Certifying Authority, shall be satisfied that the operation of an individual piece of equipment or operation of equipment in combination will not exceed more than 5dB(A) above the background level during the day when measured at the site’s boundaries and shall not exceed the background level at night (10.00pm –6.00 am) when measured at the boundary of the site.

C1. Note: A certificate from an appropriately qualified acoustic engineer is to be submitted with the Construction Certificate, certifying that all mechanical ventilation equipment or other noise generating plant in isolation or in combination with other plant will comply with the above requirements.

Reason: To comply with best practice standards for residential acoustic amenity.

30. Location of plant

Prior to the issue of the Construction Certificate, the Certifying Authority shall be satisfied that all plant and equipment (including but not limited to air conditioning equipment) is located within the basement.

C1. Note: Architectural plans identifying the location of all plant and equipment shall be provided to the Certifying Authority.

Reason: To minimise impact on surrounding properties, improved visual appearance and amenity for locality.

31. Driveway crossing levels

Prior to issue of the Construction Certificate, driveway and associated footpath levels for any new, reconstructed or extended sections of driveway crossings between the property boundary and road alignment must be obtained from Ku-ring-gai Council. Such levels are only able to be issued by Council under the Roads Act 1993. All footpath crossings, laybacks and driveways are to be constructed according to Council's specifications "Construction of Gutter Crossings and Footpath Crossings".

Specifications are issued with alignment levels after completing the necessary application form at Customer Services and payment of the assessment fee. When completing the request for driveway levels application from Council, the applicant must attach a copy of the relevant development application drawing which indicates the position and proposed level of the proposed driveway at the boundary alignment.

This development consent is for works wholly within the property. Development consent does not imply approval of footpath or driveway levels, materials or location within the road reserve, regardless of whether this information is shown on the development application plans. The grading of such footpaths or driveways outside the property shall comply with Council's standard requirements. The suitability of the grade of such paths or driveways inside the property is the sole responsibility of the applicant and the required alignment levels fixed by Council may impact upon these levels.

The construction of footpaths and driveways outside the property in materials other than those approved by Council is not permitted.

Reason: To provide suitable vehicular access without disruption to pedestrian and vehicular traffic.

32. Driveway grades – basement carparks

Prior to the issue of the Construction Certificate, longitudinal driveway sections are to be prepared by a qualified civil/traffic engineer and be submitted for to and approved by the Certifying Authority. These profiles are to be at 1:100 scale along both edges of the proposed driveway, starting from the centreline of the frontage street carriageway to the proposed basement floor level. The traffic engineer shall provide specific written certification on the plans that:

· vehicular access can be obtained using grades of 20% (1 in 5) maximum and · all changes in grade (transitions) comply with Australian Standard 2890.1 –“Off-street car parking” (refer clause 2.5.3) to prevent the scraping of the underside of vehicles.

If a new driveway crossing is proposed, the longitudinal sections must incorporate the driveway crossing levels as issued by Council upon prior application.

Reason: To provide suitable vehicular access without disruption to pedestrian and vehicular traffic.

33. Basement car parking details

Prior to issue of the Construction Certificate, certified parking layout plan(s) to scale showing all aspects of the vehicle access and accommodation arrangements must be submitted to and approved by the Certifying Authority. A qualified civil/traffic engineer must review the proposed vehicle access and accommodation layout and provide written certification on the plans that:

· all parking space dimensions, driveway and aisle widths, driveway grades, transitions, circulation ramps, blind aisle situations and other trafficked areas comply with Australian Standard 2890.1 – 2004 “Off-street car parking” · a clear height clearance of 2.6 metres (required under DCP40 for waste collection trucks) is provided over the designated garbage collection truck manoeuvring areas within the basement · no doors or gates are provided in the access driveways to the basement carpark which would prevent unrestricted access for internal garbage collection at any time from the basement garbage storage and collection area · the dimensions of all parking spaces, including lengths and widths, comply with the State Environmental Planning Policy for Senior Living relating to height clearances and space dimensions · the vehicle access and accommodation arrangements are to be constructed and marked in accordance with the certified plans

Reason: To ensure that parking spaces are in accordance with the approved development.

34. Drainage of paved areas

All new exposed impervious areas graded towards adjacent property and/or habitable areas are to be drained via the main drainage system. This may require the installation of suitable inlets pits, cut-off structures (e.g. kerb), and/or barriers that direct such runoff to the formal drainage system. Details of such measures shall be shown on the Construction Certificate drawings, to the satisfaction of the Certifying Authority.

Reason: To control surface run off and protect the environment.

35. Vehicular access and garaging

Driveways and vehicular access ramps must be designed not to scrape the underside of cars. In all respects, the proposed vehicle access and accommodation arrangements must be designed and constructed to comply with Australian Standard 2890.1 – 2004 “Off-Street car parking”. Details are to be provided to and approved by the Certifying Authority prior to the issue of the Construction Certificate.

Reason: To ensure that parking spaces are in accordance with the approved development.

36. Design of works in public road (Roads Act approval)

Prior to issue of the Construction Certificate, the Certifying Authority shall be satisfied that engineering plans and specifications prepared by a qualified consulting engineer have been approved by Council’s Development Engineer. The plans to be assessed must be to a detail suitable for construction issue purposes and must detail the following infrastructure works required in Wonga Wonga Street and Boomerang Street:

· Design details of the footpath on the opposite side of the road down to the intersection of Wonga Wonga Street and Ku-ring-gai Avenue · Pathway / pram ramp from the site frontage to the road · Detail design for the accessible footpath to the bus stop to demonstrate compliance with Clause 26 of the Seniors Living SEPP. Design to include provision of kerb ramps and mid-block roadway crossing on Boomerang Street. · The design is to be approved by the access consultant. Any works within tree protection zones shall be endorsed by a qualified arborist.

Development consent does not give approval to these works in the road reserve. The applicant must obtain a separate approval under sections 138 and 139 of The Roads Act 1993 for the works in the road reserve required as part of the development. The Construction Certificate must not be issued, and these works must not proceed until Council has issued a formal written approval under the Roads Act 1993.

The required plans and specifications are to be designed in accordance with the General Specification for the Construction of Road and Drainage Works in Ku-ring-gai Council, dated November 2004. The drawings must detail existing utility services and trees affected by the works, erosion control requirements and traffic management requirements during the course of works. Survey must be undertaken as required. Traffic management is to be certified on the drawings as being in accordance with the documents SAA HB81.1 – 1996 – Field Guide for Traffic Control at Works on Roads – Part 1 and RTA Traffic Control at Work Sites (1998). Construction of the works must proceed only in accordance with any conditions attached to the Roads Act approval issued by Council.

A minimum of three (3) weeks will be required for Council to assess the Roads Act application. Early submission of the Roads Act application is recommended to avoid delays in obtaining a Construction Certificate. An engineering assessment and inspection fee (set out in Council’s adopted fees and charges) is payable and Council will withhold any consent and approved plans until full payment of the correct fees. Plans and specifications must be marked to the attention of Council’s Development Engineers. In addition, a copy of this condition must be provided, together with a covering letter stating the full address of the property and the accompanying DA number.

Reason: To ensure that the plans are suitable for construction purposes.

37. Utility provider requirements

Prior to issue of the Construction Certificate, the applicant must make contact with all relevant utility providers whose services will be impacted upon by the development. A written copy of the requirements of each provider, as determined necessary by the Certifying Authority, must be obtained. All utility services or appropriate conduits for the same must be provided by the developer in accordance with the specifications of the utility providers.

Reason: To ensure compliance with the requirements of relevant utility providers.

38. Underground services

All electrical services (existing and proposed) shall be undergrounded from the proposed building on the site to the appropriate power pole(s) or other connection point. Undergrounding of services must not disturb the root system of existing trees and shall be undertaken in accordance with the requirements of the relevant service provided. Documentary evidence that the relevant service provider has been consulted and that their requirements have been met are to be provided to the Certifying Authority prior to the issue of the Construction Certificate. All electrical and telephone services to the subject property must be placed underground and any redundant poles are to be removed at the expense of the applicant.

Reason: To provide infrastructure that facilitates the future improvement of the streetscape by relocation of overhead lines below ground.

Conditions to be satisfied prior to the issue of the construction certificate or prior to demolition, excavation or construction (whichever comes first):

39. Infrastructure restorations fee

To ensure that damage to Council Property as a result of construction activity is rectified in a timely matter:

a) All work or activity taken in furtherance of the development the subject of this approval must be undertaken in a manner to avoid damage to Council Property and must not jeopardise the safety of any person using or occupying the adjacent public areas.

b) The applicant, builder, developer or any person acting in reliance on this approval shall be responsible for making good any damage to Council Property, and for the removal from Council Property of any waste bin, building materials, sediment, silt, or any other material or article.

c) The Infrastructure Restoration Fee must be paid to the Council by the applicant prior to both the issue of the Construction Certificate and the commencement of any earthworks or construction.

d) In consideration of payment of the Infrastructure Restorations Fee, Council will undertake such inspections of Council Property as Council considers necessary and also undertake, on behalf of the applicant, such restoration work to Council Property, if any, that Council considers necessary as a consequence of the development. The provision of such restoration work by the Council does not absolve any person of the responsibilities contained in (a) to (b) above. Restoration work to be undertaken by the Council referred to in this condition is limited to work that can be undertaken by Council at a cost of not more than the Infrastructure Restorations Fee payable pursuant to this condition.

e) In this condition:

“Council Property” includes any road, footway, footpath paving, kerbing, guttering, crossings, street furniture, seats, letter bins, trees, shrubs, lawns, mounds, bushland, and similar structures or features on any road or public road within the meaning of the Local Government Act 1993 (NSW) or any public place; and

“Infrastructure Restoration Fee” means the Infrastructure Restorations Fee calculated in accordance with the Schedule of Fees & Charges adopted by Council as at the date of payment and the cost of any inspections required by the Council of Council Property associated with this condition.

Reason: To maintain public infrastructure.

40. Section 94 Contributions

This development is subject to a development contribution calculated in accordance with Ku-ring-gai Contributions Plan 2010, being a s94 Contributions Plan in effect under the Environmental Planning and Assessment Act, as follows:

The contribution shall be paid to Council prior to the issue of any Construction Certificate, Linen Plan, Certificate of Subdivision or Occupation Certificate whichever comes first in accordance with Ku-ring-gai Contributions Plan 2010.

The contributions specified above are subject to indexation and will continue to be indexed to reflect changes in the consumer price index and housing price index until they are paid in accordance with Ku-ring-gai Contributions Plan 2010 to reflect changes in the consumer price index and housing price index. Prior to payment, please contact Council directly to verify the current payable contributions.

Copies of Council’s Contribution Plans can be viewed at Council Chambers, 818 Pacific Hwy Gordon or on Council’s website at www.kmc.nsw.gov.au.

Reason: To ensure the provision, extension or augmentation of the Key Community Infrastructure identified in Ku-ring-gai Contributions Plan 2010 that will, or is likely to be, required as a consequence of the development.

Conditions to be satisfied during the demolition, excavation and construction phases:

41. Prescribed conditions

The applicant shall comply with any relevant prescribed conditions of development consent under clause 98 of the Environmental Planning and Assessment Regulation. For the purposes of section 80A (11) of the Environmental Planning and Assessment Act, the following conditions are prescribed in relation to a development consent for development that involves any building work:

· The work must be carried out in accordance with the requirements of the Building Code of Australia · In the case of residential building work for which the Home Building Act 1989 requires there to be a contract of insurance in force in accordance with Part 6 of that Act, that such a contract of insurance is in force before any works commence.

Reason: Statutory requirement.

42. Hours of work

Demolition, excavation, construction work and deliveries of building material and equipment must not take place outside the hours of 7.00am to 5.00pm Monday to Friday and 8.00am to 12 noon Saturday. No work and no deliveries are to take place on Sundays and public holidays.

Excavation or removal of any materials using machinery of any kind, including compressors and jack hammers, must be limited to between 7.30am and 5.00pm Monday to Friday, with a respite break of 45 minutes between 12 noon 1.00pm.

Where it is necessary for works to occur outside of these hours (ie) placement of concrete for large floor areas on large residential/commercial developments or where building processes require the use of oversized trucks and/or cranes that are restricted by the RTA from travelling during daylight hours to deliver, erect or remove machinery, tower cranes, pre-cast panels, beams, tanks or service equipment to or from the site, approval for such activities will be subject to the issue of an "outside of hours works permit" from Council as well as notification of the surrounding properties likely to be affected by the proposed works.

Note: Failure to obtain a permit to work outside of the approved hours will result in on the spot fines being issued.

Reason: To ensure reasonable standards of amenity for occupants of neighbouring properties.

43. Temporary irrigation

Temporary irrigation within the Tree Protection Fencing is to be provided. Irrigation volumes are to be determined by the Project Arborist.

Reason: To protect trees to be retained on site.

44. Approved plans to be on site

A copy of all approved and certified plans, specifications and documents incorporating conditions of consent and certification (including the Construction Certificate if required for the work) shall be kept on site at all times during the demolition, excavation and construction phases and must be readily available to any officer of Council or the Principal Certifying Authority.

Reason: To ensure that the development is in accordance with the determination.

45. Statement of compliance with Australian Standards

The demolition work shall comply with the provisions of Australian Standard AS2601: 2001 The Demolition of Structures. The work plans required by AS2601: 2001 shall be accompanied by a written statement from a suitably qualified person that the proposal contained in the work plan comply with the safety requirements of the Standard. The work plan and the statement of compliance shall be submitted to the satisfaction of the Principal Certifying Authority prior to the commencement of any works.

Reason: To ensure compliance with the Australian Standards.

46. Site notice

A site notice shall be erected on the site prior to any work commencing and shall be displayed throughout the works period.

The site notice must:

· be prominently displayed at the boundaries of the site for the purposes of informing the public that unauthorised entry to the site is not permitted · display project details including, but not limited to the details of the builder, Principal Certifying Authority and structural engineer · be durable and weatherproof · display the approved hours of work, the name of the site/project manager, the responsible managing company (if any), its address and 24 hour contact phone number for any inquiries, including construction/noise complaint are to be displayed on the site notice · be mounted at eye level on the perimeter hoardings/fencing and is to state that unauthorised entry to the site is not permitted

Reason: To ensure public safety and public information.

47. Dust control

During excavation, demolition and construction, adequate measures shall be taken to prevent dust from affecting the amenity of the neighbourhood. The following measures must be adopted:

· physical barriers shall be erected at right angles to the prevailing wind direction or shall be placed around or over dust sources to prevent wind or activity from generating dust · earthworks and scheduling activities shall be managed to coincide with the next stage of development to minimise the amount of time the site is left cut or exposed · all materials shall be stored or stockpiled at the best locations · the ground surface should be dampened slightly to prevent dust from becoming airborne but should not be wet to the extent that run-off occurs · all vehicles carrying spoil or rubble to or from the site shall at all times be covered to prevent the escape of dust · all equipment wheels shall be washed before exiting the site using manual or automated sprayers and drive-through washing bays · gates shall be closed between vehicle movements and shall be fitted with shade cloth · cleaning of footpaths and roadways shall be carried out daily

Reason: To protect the environment and amenity of surrounding properties.

48. Post-construction dilapidation report

The applicant shall engage a suitably qualified person to prepare a post construction dilapidation report at the completion of the construction works. This report is to ascertain whether the construction works created any structural damage to adjoining buildings, infrastructure and roads. The report is to be submitted to the Principal Certifying Authority. In ascertaining whether adverse structural damage has occurred to adjoining buildings, infrastructure and roads, the Principal Certifying Authority must:

· compare the post-construction dilapidation report with the pre-construction dilapidation report · have written confirmation from the relevant authority that there is no adverse structural damage to their infrastructure and roads.

A copy of this report is to be forwarded to Council at the completion of the construction works.

Reason: Management of records.

49. Compliance with submitted geotechnical report

A contractor with specialist excavation experience must undertake the excavations for the development and a suitably qualified and consulting geotechnical engineer must oversee excavation.

Geotechnical aspects of the development work, namely:

· appropriate excavation method and vibration control · support and retention of excavated faces · hydro-geological considerations

must be undertaken in accordance with the recommendations of the geotechnical report 12097/GK/1, dated September 2012, prepared by GDK, Keighran Geotechnics. Approval must be obtained from all affected property owners, including Ku-ring-gai Council, where rock anchors (both temporary and permanent) are proposed below adjoining property(ies).

Reason: To ensure the safety and protection of property.

50. Use of road or footpath

During excavation, demolition and construction phases, no building materials, plant or the like are to be stored on the road or footpath without written approval being obtained from Council beforehand. The pathway shall be kept in a clean, tidy and safe condition during building operations. Council reserves the right, without notice, to rectify any such breach and to charge the cost against the applicant/owner/builder, as the case may be.

Reason: To ensure safety and amenity of the area.

51. Toilet facilities

During excavation, demolition and construction phases, toilet facilities are to be provided, on the work site, at the rate of one toilet for every 20 persons or part of 20 persons employed at the site.

Reason: Statutory requirement.

52. Protection of public places

If the work involved in the erection, demolition or construction of the development is likely to cause pedestrian or vehicular traffic in a public place to be obstructed or rendered inconvenient, or building involves the enclosure of a public place, a hoarding or fence must be erected between the work site and the public place.

If necessary, a hoarding is to be erected, sufficient to prevent any substance from, or in connection with, the work falling into the public place.

The work site must be kept lit between sunset and sunrise if it is likely to be hazardous to persons in the public place.

Any hoarding, fence or awning is to be removed when the work has been completed.

Reason: To protect public places.

53. Recycling of building material (general)

During demolition and construction, the Principal Certifying Authority shall be satisfied that building materials suitable for recycling have been forwarded to an appropriate registered business dealing in recycling of materials. Materials to be recycled must be kept in good order.

Reason: To facilitate recycling of materials.

54. Construction signage

All construction signs must comply with the following requirements:

· are not to cover any mechanical ventilation inlet or outlet vent · are not illuminated, self-illuminated or flashing at any time · are located wholly within a property where construction is being undertaken · refer only to the business(es) undertaking the construction and/or the site at which the construction is being undertaken · are restricted to one such sign per property · do not exceed 2.5m2 · are removed within 14 days of the completion of all construction works

Reason: To ensure compliance with Council's controls regarding signage.

55. Road reserve safety

All public footways and roadways fronting and adjacent to the site must be maintained in a safe condition at all times during the course of the development works. Construction materials must not be stored in the road reserve. A safe pedestrian circulation route and a pavement/route free of trip hazards must be maintained at all times on or adjacent to any public access ways fronting the construction site. Where public infrastructure is damaged, repair works must be carried out when and as directed by Council officers. Where pedestrian circulation is diverted on to the roadway or verge areas, clear directional signage and protective barricades must be installed in accordance with AS1742-3 (1996) “Traffic Control Devices for Work on Roads”. If pedestrian circulation is not satisfactorily maintained across the site frontage, and action is not taken promptly to rectify the defects, Council may undertake proceedings to stop work.

Reason: To ensure safe public footways and roadways during construction.

56. Services

Where required, the adjustment or inclusion of any new utility service facilities must be carried out by the applicant and in accordance with the requirements of the relevant utility authority. These works shall be at no cost to Council. It is the applicants’ full responsibility to make contact with the relevant utility authorities to ascertain the impacts of the proposal upon utility services (including water, phone, gas and the like). Council accepts no responsibility for any matter arising from its approval to this application involving any influence upon utility services provided by another authority.

Reason: Provision of utility services.

57. Erosion control

Temporary sediment and erosion control and measures are to be installed prior to the commencement of any works on the site. These measures must be maintained in working order during construction works up to completion. All sediment traps must be cleared on a regular basis and after each major storm and/or as directed by the Principal Certifying Authority and Council officers.

Reason: To protect the environment from erosion and sedimentation.

58. Drainage to street

Stormwater runoff from all new impervious areas and subsoil drainage systems shall be piped to the street drainage system. New drainage line connections to the street drainage system shall conform and comply with the requirements of Sections 5.3 and 5.4 of Ku-ring-gai Water Management Development Control Plan No. 47.

Reason: To protect the environment.

59. Grated drain at garage

A 200mm wide grated channel/trench drain, with a heavy-duty removable galvanised grate is to be provided in front of the garage door/basement parking slab to collect driveway runoff. The channel drain shall be connected to the main drainage system and must have an outlet of minimum diameter 150mm to prevent blockage by silt and debris.

Reason: Stormwater control.

60. Sydney Water Section 73 Compliance Certificate

The applicant must obtain a Section 73 Compliance Certificate under the Sydney Water Act 1994. An application must be made through an authorised Water Servicing Co-ordinator. The applicant is to refer to “Your Business” section of Sydney Water’s web site at www.sydneywater.com.au then the “e-develop” icon or telephone 13 20 92. Following application a “Notice of Requirements” will detail water and sewer extensions to be built and charges to be paid. Please make early contact with the Co-ordinator, since building of water/sewer extensions can be time consuming and may impact on other services and building, driveway or landscape design.

Reason: Statutory requirement.

61. Arborist’s report

The trees to be retained shall be inspected, monitored and treated by a Project Arborist who must be a qualified (AQF) Level 5 arborist in accordance with AS4970-2009 Protection of trees on development sites. Regular inspections and documentation from the Project Arborist to the Principal Certifying Authority are required including at the following times or phases of work. All monitoring shall be recorded and provided to the Principal Certifying Authority prior to completion of the works.

Reason: To ensure protection of existing trees.

62. Canopy/root pruning

Canopy and/or root pruning of the following tree(s) which is necessary to accommodate the approved building works shall be undertaken by an experienced AQF level 3 Arborist under the supervision of the Project Arborist and in accordance with the reduction pruning clause of AS4373-2007. All other branches are to be tied back and protected during construction, under the supervision of a qualified arborist.

Reason: To protect the environment.

63. Treatment of tree roots

If tree roots are required to be severed for the purposes of constructing the approved works, they shall be cut cleanly by hand, by an experienced Arborist/Horticulturist with a minimum qualification of Horticulture Certificate or Tree Surgery Certificate. All pruning works shall be undertaken as specified in Australian Standard 4373-2007 – Pruning of Amenity Trees.

Reason: To protect existing trees.

64. Hand excavation

All excavation (excluding for the basement) within the specified radius of the trunk(s) of the following tree(s) shall be hand dug under the supervision of the Project Arborist.

Reason: To protect existing trees.

65. No storage of materials beneath trees

No activities, storage or disposal of materials shall take place beneath the canopy of any tree protected under Council's Tree Preservation Order at any time.

Reason: To protect existing trees.

66. Removal of refuse

All builders' refuse, spoil and/or material unsuitable for use in landscape areas shall be removed from the site on completion of the building works.

Reason: To protect the environment.

67. Canopy replenishment trees to be planted

The canopy replenishment trees to be planted shall be maintained in a healthy and vigorous condition until they attain a height of 5.0 metres whereby they will be protected by Council’s Tree Preservation Order. Any of the trees found faulty, damaged, dying or dead shall be replaced with the same species.

Reason: To maintain the treed character of the area.

68. On site retention of waste dockets

All demolition, excavation and construction waste dockets are to be retained on site, or at suitable location, in order to confirm which facility received materials generated from the site for recycling or disposal.

· Each docket is to be an official receipt from a facility authorised to accept the material type, for disposal or processing. · This information is to be made available at the request of an Authorised Officer of Council.

Reason: To protect the environment.

Conditions to be satisfied prior to the issue of an Occupation Certificate:

69. Compliance with BASIX Certificate

Prior to the issue of an Occupation Certificate, the Principal Certifying Authority shall be satisfied that all commitments listed in BASIX Certificate No.440332M_04 have been complied with.

Reason: Statutory requirement.

70. Clotheslines and clothes dryers

Prior to the issue of the Occupation Certificate, the Principal Certifying Authority shall be satisfied that the units either have access to an external clothes line located in common open space or have a mechanical clothes dryer installed.

Reason: To provide access to clothes drying facilities.

71. Mechanical ventilation

Following completion, installation and testing of all the mechanical ventilation systems, the Principal Certifying Authority shall be satisfied of the following prior to the issue of any Occupation Certificate:

1. The installation and performance of the mechanical systems complies with:

· The Building Code of Australia · Australian Standard AS1668 · Australian Standard AS3666 where applicable

2. The mechanical ventilation system in isolation and in association with other mechanical ventilation equipment, when in operation will not be audible within a habitable room in any other residential premises before 7am and after 10pm Monday to Friday and before 8am and after 10pm Saturday, Sunday and public holidays. The operation of the unit outside these restricted hours shall emit a noise level of not greater than 5dbA above the background when measured at the nearest adjoining boundary.

Note: Written confirmation from an acoustic engineer that the development achieves the above requirements is to be submitted to the Principal Certifying Authority prior to the issue of the Occupation Certificate.

Reason: To protect the amenity of surrounding properties.

72. Completion of landscape works

Prior to the release of the Occupation Certificate, the Principal Certifying Authority is to be satisfied that all landscape works, including the removal of all noxious and/or environmental weed species, have been undertaken in accordance with the approved plan(s) and conditions of consent.

Reason: To ensure that the landscape works are consistent with the development consent.

73. Completion of tree works